Table of Contents

Most people put off buying life insurance not because they don’t care but because they don’t know where to start. And the biggest question that stops them is simple. How much life insurance do I need?

It’s a fair question. And once you get a real answer it stops feeling overwhelming.

This blog walks you through every method every factor and every life situation you need to think about before you pick a coverage amount. By the end you’ll know exactly how to use a life insurance calculator to get your number.

What Does “How Much Life Insurance Do I Need” Really Mean?

It’s Really About the Death Benefit, Not the Policy

Here’s the thing. When people ask how much life insurance do I need what they’re really asking is how large should my death benefit be. The death benefit is the amount of money your family receives when you pass. It’s the core of any life policy. The type of policy you pick matters but the number matters more.

Think about what your family would actually need if you weren’t there tomorrow. They’d need to cover rent or mortgage payments. They’d need to replace your annual income. They’d need to handle final expenses and maybe college costs for the kids. That total number is your death benefit target and that’s what the life insurance calculator helps you figure out.

Factors That Determine How Much Life Insurance You Need

No two people have the same life insurance need. The right amount of life insurance depends on your personal financial picture. A few key factors shape the coverage you need more than anything else.

| Factor | Why It Affects Your Coverage Amount |

|---|---|

| Annual Income | Determines how much your family needs to replace |

| Outstanding Debts | Mortgage, loans and credit cards your family would inherit |

| Number of Dependents | More dependents means more years of support needed |

| Existing Savings | Higher savings reduce the gap in coverage |

| Age & Health | Affects policy type and how long coverage is needed |

| Existing Life Insurance | Group life insurance or other policies offset the total need |

Your Income and How Long Your Family Needs It

Your annual income is the starting point for any coverage calculation. The whole point of life insurance is to replace the money your family depends on day to day.

Ask yourself this. If you were gone how many years would your family need financial support? Most families need living expenses covered for at least 10 to 20 years depending on the age of your kids and your spouse’s earning ability. Your life insurance income multiple starts right here.

Outstanding Debts Mortgage, Loans and Credit Cards

Your family shouldn’t have to sell the house or drain savings just to stay afloat. A solid life insurance coverage amount accounts for your mortgage balance plus any car loans student loans and credit card balances you carry.

If you pass without enough insurance coverage those debts don’t disappear. They fall on the people you leave behind. That’s why outstanding debt is one of the first things to factor in when calculating your life insurance needs.

Future Needs College, Final Expenses and Retirement Support

College costs add up fast especially if you have more than one child. Per child estimates for a four year degree can be significant depending on the school and state. Beyond that your family will face final expenses like funeral costs which typically run several thousand dollars.

If your spouse is close to retirement age life insurance proceeds can also help bridge the gap between their current savings and what they’ll actually need. These future costs are easy to forget but they’re a real part of determining your life insurance needs.

Existing Savings and Current Life Insurance to Offset the Need

You don’t need life insurance to cover every dollar from scratch. If you already have solid savings a retirement account or existing life insurance policies like group life insurance through work some of that can count toward your total.

Subtract what you already have from what your family would need. That gap is the life insurance amount you actually need to buy. A financial advisor can help you run this math cleanly if your situation is complicated.

How Much Life Insurance Do I Need Calculator How to Use It

Why Using a Life Insurance Calculator Beats Guessing

A lot of people just guess. They pick a round number like $500,000 and hope it’s enough. But guessing can leave your family short or cost you more than you need to spend on premiums.

A life insurance calculator removes the guesswork. It takes your income your debts your dependents and your existing assets and spits out an actual number based on your real situation. That’s a much smarter starting point than guessing. Our life insurance premium calculator does exactly that and it takes less than two minutes.

What Information You Need Before Using Our Life Insurance Calculator

Before you open the life insurance calculator pull together a few things. You’ll want to know your annual income your total mortgage balance any other debts you carry and how many dependents you have.

It also helps to know whether you have any existing life insurance policies and what your savings look like. The more accurate the inputs the closer the result will be to what you actually need. Think of it as a life insurance worksheet calculator you fill in once and get real clarity fast.

4 Methods to Estimate How Much Life Insurance You Need

There’s no single right way to estimate how much life insurance you need. Different methods work better for different situations. Here are the four most widely used approaches.

| Method | Formula | Best For | Limitation |

|---|---|---|---|

| Income x 10 | Annual income × 10 | Quick baseline estimate | Doesn’t account for debts or kids |

| Income x 10 + College | Income × 10 + college costs per child | Families with children | Still misses mortgage and other debts |

| Income x 15 | Annual income × 15 | Conservative long term planning | May overestimate for some households |

| DIME Method | Debt + Income + Mortgage + Education | Detailed and personalized | Takes more time to calculate |

Income x 10 The Simplest Life Insurance Rule of Thumb

The most basic life insurance rule of thumb is to multiply your annual income by 10. So if you earn $70,000 a year you’d aim for $700,000 in coverage. It’s a fast starting point. And it works well if you don’t have heavy debts or kids in school. But it doesn’t account for your mortgage or your specific coverage needs so treat it as a floor not a ceiling. If your situation is more complex you’ll want to go further.

Income x 10 Plus College Estimate How Much Life Insurance You Need With Kids

This variation takes the basic income multiple and adds college costs on top. The idea is to multiply your income by 10 and then add roughly the projected cost of a four year degree for each child you have.

For two kids that number goes up noticeably. It’s a better fit for young families because it directly addresses child care and education costs that the basic income multiple leaves out. It’s still not the most detailed method but it gets you closer to the real coverage you need.

Income x 15 A More Conservative Life Insurance Income Multiple

Some financial planners suggest bumping the multiplier to 15 instead of 10. This life insurance income multiple builds in a bigger buffer for inflation longer income replacement periods and unexpected costs. If you’re the sole earner in your household or your family has higher living expenses the x15 method gives you more breathing room. It’s a simple tweak to the basic rule that makes a real difference in long term protection.

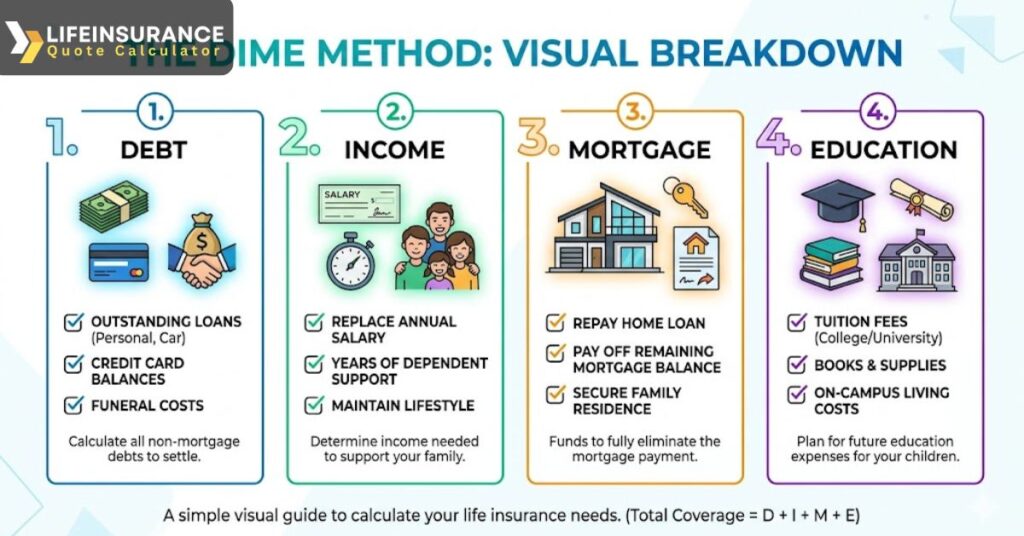

The DIME Method Life Insurance Calculator The Most Detailed Approach

The DIME method life insurance calculator is the most thorough way to calculate how much life insurance you need. It stands for Debt, Income, Mortgage and Education. Each piece gets its own number and you add them all together.

| DIME Component | What to Include | Example |

|---|---|---|

| Debt | All non mortgage debts car loans, credit cards, student loans | Total outstanding balances |

| Income | Annual income × number of years family needs support | Years until youngest child is self sufficient |

| Mortgage | Full remaining balance on your home loan | Current payoff amount |

| Education | Projected college cost per child | Total for all children |

The result is a highly personalized life insurance amount. It takes a bit more time to fill out but it gives you a much clearer picture of the right amount of life insurance for your specific household. Many people are surprised by how different the DIME number is compared to a simple income multiple.

The Human Life Value Method Determining Your Life Insurance Needs Precisely

How to Calculate Human Life Value for Life Insurance

Human life value is an older actuarial concept but it’s one of the most accurate ways to put a number on your financial worth to your family. The idea is to calculate the present value of everything you’d earn between now and retirement. You take your annual income subtract your personal living expenses and then multiply that figure by the number of working years you have left.

The result is your human life value and it represents the total economic loss your family would face if you passed today. It’s more math heavy than other methods. But for people with high incomes long careers ahead or complex financial situations it produces the most precise life insurance coverage amount.

Who Should Use the Human Life Value Method to Determine How Much Life Insurance

Not everyone needs this level of detail. But if you’re a high earner a business owner or someone with a long career ahead the human life value method gives you a number that actually reflects what your family stands to lose.

It’s also a good check on other estimates. If your DIME number and your human life value number are in the same ballpark you can feel confident in your target range. A financial advisor can walk you through this calculation if the math feels like a lot to take on alone.

How Much Life Insurance Do I Need by Age

Your life insurance needs by age shift a lot over the years. What makes sense at 25 looks very different at 60. Here’s a breakdown of how the right amount of life insurance tends to shift across different life stages.

| Age Group | Typical Coverage Recommendation | Key Reason |

|---|---|---|

| Age 25 | 10–15x income | Early career, few assets, low cost to lock in coverage |

| Age 30–40 | 10–15x income + debts + kids | Peak earning years, mortgage, growing family |

| Age 40 | 10x income + full debt review | Mid career, college costs becoming real |

| Age 50 | 7–10x income | Kids growing up, mortgage shrinking, savings building |

| Age 55 | 5–7x income | Pre retirement, reduced obligations |

| Age 60 | Targeted coverage for final expenses and estate | Focus shifts to legacy and end of life costs |

How Much Life Insurance Do I Need at 25

At 25 your biggest asset is time. Buying life insurance young locks in low rates and covers the debts you’re starting to build. You may not have dependents yet but if you have student loans or co signed debt someone else could be on the hook.

The minimum life insurance coverage at this age is usually enough to cover your debts and at least a few years of income. If you do have a partner or young family that number goes up. A term life insurance policy is almost always the most practical fit here.

How Much Life Insurance Do I Need at 40

By 40 most people are carrying a mortgage raising kids and sitting at peak earning years. This is where the gap between what you have and what your family need to replace is usually the widest.

A solid rule of thumb at this age is 10x your income plus your full mortgage balance plus projected college costs for each child. If you haven’t reviewed your coverage since you were younger now is the time. Life insurance needs change and your 40s are when that really shows up.

How Much Life Insurance Do I Need at 50

At 50 the picture starts to shift. Your kids may be finishing school. Your mortgage balance is lower. Your savings are hopefully stronger. That means the amount of life insurance you need starts to come down for most people.

That said you still want enough to replace income for your spouse cover any remaining debts and handle final expenses. Don’t assume your group life insurance at work is enough. Check the actual numbers.

How Much Life Insurance Do I Need at 55

At 55 you’re in the home stretch of your working years. Your coverage needs are more focused now. The goal is making sure your spouse can maintain their lifestyle and that final expenses won’t be a burden.

Life insurance needs by age at this point lean more toward targeted coverage rather than large income replacement blocks. Many people at 55 reduce their term coverage and focus on what a permanent life insurance policy can do for their estate.

How Much Life Insurance Do I Need at 60

At 60 the question shifts from income replacement to legacy and final expenses. Your kids are likely grown. Your debts are smaller. But your spouse may still depend on your income or pension.

A smaller focused policy can cover final expenses estate costs and provide some support for a surviving spouse. It’s also a good time to talk to a financial advisor about how your life insurance proceeds fit into your broader financial plan.

Life Insurance Needs for Special Situations

How Much Life Insurance Do I Need as a Single Person

Single people often think they don’t need life insurance at all. But that’s not always true. If you have debt that a co signer could inherit or if you’re supporting a parent or sibling some amount of insurance still makes sense.

At a minimum minimum life insurance coverage for a single person should cover outstanding debts and final expenses. If no one depends on your income financially a smaller term life insurance policy is usually enough to cover the basics.

Life Insurance for a Stay at Home Parent Why Coverage Still Matters

Life insurance for stay at home parent is one of the most overlooked areas in family financial planning. Because a stay at home parent doesn’t bring in a paycheck people assume they don’t need coverage. That’s a real mistake.

Child care alone can cost a significant amount per year. Add in cooking cleaning household management and the daily support that keeps everything running and you’re looking at a substantial economic contribution. Life insurance to cover that cost matters and it should be part of every family’s financial plan.

Life Insurance for Income Replacement Protecting Your Family’s Monthly Budget

The main job of life insurance for income replacement is to make sure your family can keep paying the bills after you’re gone. Rent or mortgage utilities groceries child care and everything else that comes out of your paycheck every month.

Insurance needs is to multiply your income by the number of years your family would need support and that gives you a baseline. Then add debts and future costs on top. That’s how you get from a vague idea to an actual number your family can count on.

Using Life Insurance in an Estate or Business Plan

Life insurance proceeds can do more than just replace income. They can fund a business buyout cover estate taxes or create a legacy for your children. This is where permanent life insurance policies and whole life policies often come into play.

If your financial plan includes business succession or estate transfer a financial advisor can help you structure the right life policy for those goals. The death benefit becomes a planning tool not just a safety net.

Term Life Insurance vs. Whole Life Insurance Which One Fits Your Need

When you’re purchasing life insurance one of the first choices you’ll face is between term life insurance and whole life insurance. Both are real types of life insurance with different purposes and different fits.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Duration | Fixed period (10, 20 or 30 years) | Lifetime coverage |

| Monthly Cost | Lower | Higher |

| Cash Value | No | Yes builds over time |

| Best For | Income replacement, mortgage protection | Estate planning, long term wealth building |

| Flexibility | Can convert in many cases | Fixed premium structure |

When Term Life Insurance Covers Your Life Insurance Needs Best

A term life insurance policy is the right fit for most working families. It covers you during the years your family depends on your income the most. When the youngest child graduates high school and your mortgage is nearly paid off the need for large coverage drops naturally.

Much term life coverage is far less expensive than whole life for the same death benefit. So if your goal is pure income replacement and debt protection a term insurance policy is almost always the smarter financial move. It keeps more money in your pocket while still giving your family real protection.

When Whole Life Insurance Makes Sense for Long Term Life Insurance Needs

Whole life insurance makes more sense when your goal goes beyond basic income replacement. If you want coverage that never expires builds cash value over time and plays a role in your estate plan then whole life policies are worth a closer look.

Permanent life insurance is also a fit if you have a dependent with a lifelong disability or if you’re using life insurance proceeds as part of a business succession plan. It costs more but it does more. The key is making sure the higher cost fits your actual financial plan and not just a sales pitch.

How Life Insurance Needs Change Over Time

Life Events That Should Trigger a Coverage Review

Life insurance needs change and they change faster than most people expect. Getting married having a child buying a house getting a raise or losing a spouse are all moments when your existing coverage might no longer match your real situation.

Different life stages bring different financial responsibilities. A policy you bought at 28 when you were single might be seriously underpowered now that you have a family and a mortgage. Reviewing your life insurance coverage every two to three years or after any major life changes is a smart habit.

Minimum Life Insurance Coverage When Less Is Still Enough

Not every situation calls for a million dollar policy. For some people minimum life insurance coverage is all they actually need. If your kids are grown your home is paid off and your spouse has strong retirement savings a smaller policy focused on final expenses and a bit of income support might be the right call.

The goal is coverage that matches your actual coverage needs not coverage that looks impressive on paper. Less life insurance is better than no coverage at all and it’s better than overpaying for protection your family won’t actually need.

Determining Your Life Insurance Needs A Simple Life Insurance Worksheet Walkthrough

A life insurance worksheet calculator takes all the methods we’ve talked about and puts them into one simple fill in format. It’s the clearest way to go from general ideas to a specific life insurance amount you can actually act on.

| Line Item | Your Number |

|---|---|

| Annual income × years of support needed | $ |

| Total mortgage balance | $ |

| Other debts (car, credit cards, student loans) | $ |

| College costs per child × number of children | $ |

| Final expenses estimate | $ |

| Subtotal (add all rows above) | $ |

| Subtract existing savings and life insurance | $ |

| Coverage Gap = Amount of Life Insurance Needed | $ |

How to Calculate Life Insurance Needs Step by Step

Calculating your life insurance needs doesn’t have to be complicated. Start with your annual income and multiply by how many years your family would need support. Add your mortgage balance your other debts your projected college costs and a buffer for final expenses.

Then subtract what you already have. That means your savings your existing life insurance policies and any group life insurance your employer provides. What’s left is the gap. That gap is the amount of life insurance you need to buy and it’s the number you take into a quote. Our term life insurance calculator walks you through this step by step and gives you a real number based on your actual inputs.

How to Adjust Your Life Policy as Your Financial Situation Shifts

Your life policy shouldn’t be a set it and forget it decision. As your income grows your debts shrink and your kids grow up the amount of insurance needed changes too.

Life stages matter here. What you need to replace at 35 is very different from what you need at 55. Revisit your life insurance coverage amount guide every few years and after major financial events. Additional life insurance can be added if your needs grow and coverage can be reduced or let expire when it’s no longer needed.

Frequently Asked Questions

1. How much life insurance do I need?

The truth is this depends on your income your debts and your family needs. A simple way is using a life insurance income multiple like ten times your yearly income. When people ask how much life insurance do i need I usually say start there then adjust.

2. What is the recommended amount of life insurance?

In most cases the life insurance rule of thumb suggests eight to twelve times your income. That range works for many families. But your actual number may change based on loans kids and future plans.

3. How do you decide how much life insurance you need?

Here is the thing I often use the DIME method life insurance calculator. It looks at debt income mortgage and education. That gives a more real number than guessing and helps answer how much life insurance do i need.

4. How much life insurance is enough?

Enough means your family can pay bills and live without stress. It should cover income for years and clear major debts. A good life insurance coverage amount guide can help you fine tune this.

5. Is 500000 life insurance enough?

For some people it works. For others it falls short. If your income is high or you have kids then it may not be enough. I have seen cases where 500000 barely covered a mortgage.

6. How much life insurance do I need in my 20s?

In your 20s you can keep it simple. A lower cost term plan based on income works well. Life insurance needs by age are usually lower here unless you have dependents.

7. How much life insurance do I need at 60?

At 60 your focus shifts. You may only need enough for final costs or to support a spouse. Minimum life insurance coverage is often enough if debts are low.

8. How much life insurance do I need if I have no dependents?

If no one relies on your income then you may not need much. A small policy for debts and burial costs is fine. I have seen many singles keep it basic and affordable.

9. How much life insurance do I need for a mortgage?

You should at least cover the remaining mortgage balance. That way your family can keep the home. This is one of the easiest ways to answer how much life insurance do i need.

10. How much life insurance should I take out?

So it comes down to your goals. Use a life insurance worksheet calculator and match it with your income and expenses. That usually gives a clear and practical number.

Calculate How Much Life Insurance You Need Start Here

You now have every method every factor and every life insurance coverage amount guide you need to make a smart decision. Whether you use the income multiple the DIME method or the human life value approach the goal is the same making sure your family has enough to keep going without financial stress.

The next step is simple. Use our free life insurance calculator to get your actual number. It takes under two minutes and you don’t need to give anyone your phone number to see your results. Start with our life insurance premium calculator or explore related topics like how life insurance is calculated and term vs whole life insurance to keep building your knowledge. Your family’s financial future is worth a two minute calculation. Don’t put it off any longer.

Office: 13th Analyze Street, New York, NY 10003

Phone: +1 (523) 235 0786

Email: info@lifeinsurancequotecalculator.com

Follow us on our Linkedin and Facebook!