Table of Contents

If you smoke and you’ve been putting off buying life insurance because you think it’s either too expensive or flat out impossible to get that’s actually one of the most common misconceptions out there. The truth is, life insurance for smokers is very real and very available. It’s not going to be the same as what a nonsmoker pays but it’s also not the financial wall most people imagine it to be. So let’s talk about what actually happens when a smoker applies for life insurance and what you can do to make smart choices along the way.

Can Smokers Get Life Insurance in the US?

Why Smokers Are Not Automatically Denied Coverage

Short answer no, smokers are not automatically turned away. Insurance companies look at your full health picture not just the fact that you use tobacco. A lot of people assume that the moment they check “yes” on the smoking question they’re done. But that’s not how it works at all.

Life insurance companies want your business. What they do instead of denying you outright is adjust your premium to reflect the added health risk that comes with smoking and tobacco use. So you still get life insurance you just pay more for it than nonsmokers do. And honestly for most smokers that trade off is completely worth it because the alternative is leaving your family with nothing.

Who Qualifies for Life Insurance as a Smoker

Here’s the thing almost any adult smoker in the US can qualify for life insurance in some form. Your age, your overall health and the type of policy you choose all play a role. A healthy 35 year old who smokes is going to have far more life insurance options than a 60 year old with multiple conditions on top of smoking. But even in that second case there are life insurance policies built specifically for higher risk applicants.

The key is that life insurance as a smoker is not a closed door. It’s just a different door with different terms.

How Life Insurance Companies Define and Classify Smokers

What Counts as Smoking According to Insurers

This is where a lot of people get caught off guard. When life insurance companies classify smokers they don’t just mean someone who lights up a cigarette every morning. Their definition is a lot wider than most people expect.

If you’ve used tobacco or nicotine in any form within the past 12 months sometimes even 24 months depending on the insurer you’ll likely be rated as a smoker on your life insurance application. That’s the baseline most insurance companies use. And it doesn’t matter how often you smoke. Once a week still counts.

Cigarettes, Cigars, Chewing Tobacco, E Cigarettes and Vaping How Each Is Treated

Not all tobacco products are treated equally and that’s the part most people miss. Cigarette smokers tend to get the toughest classification. But what about cigar smokers? Some insurers are actually more lenient with occasional cigar smokers specifically people who smoke one or two cigars a month. Some companies will even offer nonsmoker rates to occasional cigar smokers if there’s no nicotine detected in your system at the time of the insurance medical exam.

Chewing tobacco and smokeless tobacco are typically rated as smoker classifications as well. And e cigarette vaping life insurance is an area where companies are still figuring out their policies. Most insurance companies treat vaping the same as cigarette smoking right now because nicotine is still present. So if you’ve switched to a vape thinking it won’t count it almost certainly will.

| Tobacco Product | Typical Insurer Classification |

|---|---|

| Cigarettes | Smoker |

| Cigars (daily) | Smoker |

| Cigars (occasional) | Varies sometimes nonsmoker |

| Chewing Tobacco | Smoker |

| E Cigarettes / Vaping | Smoker (most carriers) |

| Nicotine Patches / Gum | Varies by carrier |

| Marijuana | Varies by carrier |

How Long Nicotine Stays in Your System and Why It Matters

Nicotine typically shows up in urine for 3 to 4 days after use. But cotinine which is what nicotine breaks down into can stay detectable for up to 10 days in urine and even longer in hair follicle tests. Some life insurance companies use cotinine tests specifically because they’re harder to beat with a short break from smoking.

So if you’re planning to quit before your life insurance medical exam and then restart after that’s a risk that can seriously backfire. And more on that in a bit.

How Do Life Insurance Companies Know If You Smoke?

The Nicotine Test During the Life Insurance Medical Exam

When you apply for life insurance with a medical exam the insurer will typically collect a urine or blood sample as part of the process. That sample gets tested for cotinine which is the direct byproduct of nicotine metabolism. This nicotine test life insurance process is standard and it’s accurate.

You can’t fake it by drinking extra water or skipping a few days of smoking before the test. The insurance medical exam is designed to catch exactly that. So plain and simple if you use tobacco the test is going to show it.

Prescription Databases and MIB Records Used by Insurers

Beyond the physical exam life insurance companies also pull data from two major sources. The first is the MIB which stands for the Medical Information Bureau. It’s basically a database that holds health related information from previous insurance applications. If you disclosed smoking on a past life insurance application that information is likely sitting in there.

The second source is prescription databases. If you’ve been prescribed nicotine replacement therapy like patches or gum your prescription history can signal tobacco use even if your blood test comes back clean.

What Happens If You Lie About Tobacco Use on Your Insurance Application

This is where things get serious. If you lie about smoking on your life insurance application and the insurance company finds out and they often do a couple of things can happen. During the first two years of your policy the insurer can investigate any claim and if they find misrepresentation they can deny the death benefit entirely and cancel your policy. After two years policies typically become incontestable but that doesn’t protect you if outright fraud was involved.

The bottom line is this being honest on your insurance application is always the right move. You’ll still get life insurance. It’ll just be priced accurately for who you are.

How Smoking Affects Your Life Insurance Rates

Smoker vs Non Smoker Life Insurance Rates The Real Difference

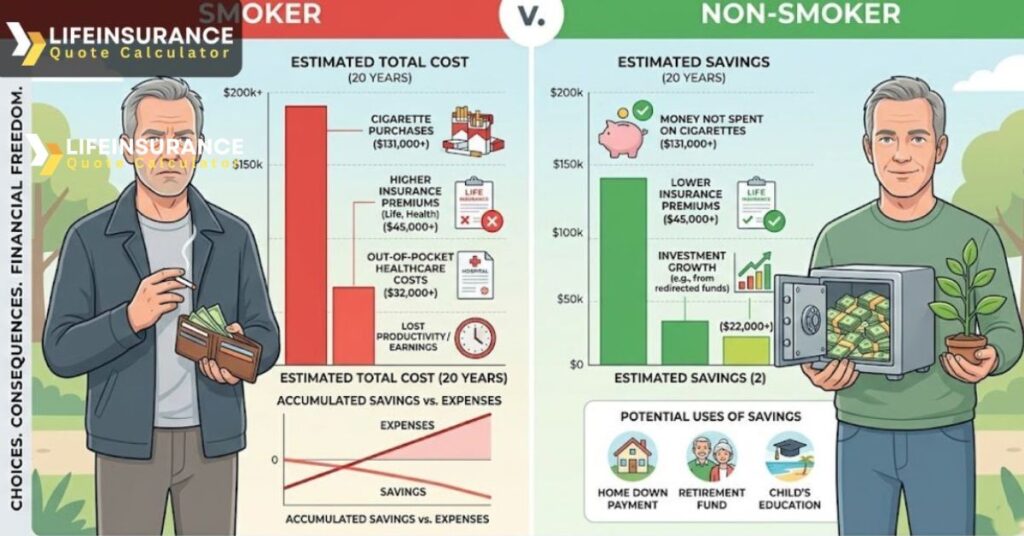

When it comes to life insurance smoker vs nonsmoker the rate gap is real and it’s noticeable. Smokers pay anywhere from two to three times more than nonsmokers for the same coverage. That’s a real difference and it comes directly from the life expectancy data that life insurance companies use to price their products.

Smoking affects life insurance rates because it statistically shortens life expectancy and raises the likelihood of serious illness. Insurance companies price life insurance rates based on risk and smokers represent a higher risk than nonsmokers by a wide margin. You can use our life insurance premium calculator to see how your smoking status affects your estimated monthly rate.

Health Risk Factors That Push Smoker Premiums Higher

It’s not just the smoking itself. Life insurance companies also look at related health risk factors when setting smoker life insurance rates. Things like blood pressure, cholesterol levels, body weight and family medical history all factor in. A smoker who is otherwise healthy will get significantly better life insurance rates than a smoker who also has high blood pressure and a family history of heart disease.

So taking care of your overall health even while you’re still a tobacco user can actually make a meaningful difference in what you pay. If you’re managing a condition like hypertension on top of smoking read our post on life insurance with high blood pressure for more detail.

How Your Smoker Health Classification Affects What You Pay

Life insurance companies classify smokers into different tiers just like they do with nonsmokers. The best tier available to a smoker is typically called Preferred Smoker. Below that you have Standard Smoker and then substandard or table rated classifications for smokers with additional health risk factors.

Getting into the preferred smoker rates tier means you’ve got solid overall health aside from the tobacco use. And that tier can save you a meaningful amount compared to a Standard Smoker rating.

| Health Class | Smoker | Non Smoker |

|---|---|---|

| Best Available | Preferred Smoker | Preferred Plus |

| Good Health | Standard Smoker | Preferred |

| Average Health | Substandard | Standard Plus |

| Higher Risk | Table Rated | Standard |

Types of Life Insurance Available to Smokers

Term Life Insurance for Smokers

Term life insurance is the most straightforward option and honestly it’s where most smokers start. A term life insurance policy covers you for a set period 10, 20 or 30 years and pays a death benefit to your family if you pass during that term. The premium stays fixed for the entire length of the term policy which makes budgeting a lot easier.

For smokers who are in otherwise decent health term life insurance tends to offer the most affordable life insurance option available. Use our term life insurance calculator to get a quick sense of what your coverage could look like. The coverage is pure protection with no cash value component which keeps the cost lower than permanent life insurance policies.

Whole Life Insurance for Smokers

Whole life insurance is permanent. It doesn’t expire as long as you keep paying the premium and it builds cash value over time that you can borrow against. For smokers the cost of whole life policies is considerably higher than term life insurance and that’s before the smoker surcharge even gets applied.

That said whole life insurance makes sense for smokers who want lifelong coverage and have estate planning needs or want to leave something behind regardless of when they pass. It’s not for everyone but it’s a solid option if the budget supports it. Check out our breakdown of term vs whole life insurance to see which one fits your situation better.

Guaranteed Issue and Simplified Issue Life Insurance for Smokers

Guaranteed issue life insurance is exactly what it sounds like. You can’t be turned down regardless of your health or smoking status. There’s no medical exam and no health questions. The trade off is that life insurance coverage amounts are lower and the premium is higher relative to the coverage you get.

Simplified issue sits between fully underwritten policies and guaranteed issue life. You answer a few health questions but there’s no insurance medical exam. Smokers who don’t want to go through a full exam process often look at simplified issue as a middle ground.

Final Expense Life Insurance for Smokers

Final expense policies are a type of life insurance designed to cover end of life costs like funeral expenses and medical bills. They’re typically smaller policies and they’re available to smokers without much hassle. Older smokers who may not qualify for life insurance through traditional underwriting often find final expense policies a practical solution.

Life Insurance for Smokers With No Medical Exam

No exam life insurance is growing fast and it’s a real option for smokers. Instead of going through a paramedical exam you answer health questions and the insurer verifies your information through databases. Smokers still get classified as tobacco users through this process the nicotine test life insurance step just gets replaced by data verification.

The upside is speed and convenience. Some policies get approved the same day. The downside is that life insurance rates through no exam carriers can be slightly higher than fully underwritten policies.

Best Life Insurance for Smokers What to Look For in a Policy

How to Compare Life Insurance Policies as a Smoker

Shopping for life insurance as a smoker means looking at more than just the monthly premium. You want to compare the death benefit amount, the length of the term life insurance policy if you’re going that route and the financial strength rating of the insurance company. A carrier with a weak financial rating might offer lower rates today but that’s not worth much if they’re not around to pay your claim.

Getting life insurance quotes from multiple insurers is the smartest starting point. Smoker life insurance rates vary a lot between carriers so comparing quotes from multiple insurers can lead to real savings without changing a thing about your coverage.

What Makes a Life Insurance Policy the Best Fit for Tobacco Users

The best life insurance for smokers is the one that fits your actual life. That means enough life insurance coverage to protect your family, a premium you can realistically keep paying and a carrier that specializes in or is friendly toward smokers and tobacco users. Some insurance companies are simply more competitive for tobacco users than others. An experienced insurance agent who works with smokers regularly can point you toward the carriers that offer the best rates for your specific profile.

How to Find the Most Affordable Life Insurance Coverage as a Smoker

Affordable life insurance as a smoker comes down to a few things. Your age matters the younger you are when you apply for life insurance the lower your smoker life insurance rates will be. Your overall health matters too. And the type of life insurance you choose plays a big role. Term life insurance is almost always going to be more affordable than whole life insurance for a smoker on a budget.

Working with an independent insurance agent who has access to multiple carriers is one of the best moves you can make. They can match your profile to the carriers most likely to give you competitive rates.

Cheapest Life Insurance for Smokers How to Lower Your Premiums

Tips That Help Smokers Reduce Their Life Insurance Costs

There are real ways to bring your smoker life insurance rates down without quitting smoking overnight. Improving other health markers helps a lot. Getting your blood pressure under control, losing weight if your BMI is on the higher side and cleaning up your driving record can all move you into a better health risk classification even as a smoker.

Buying life insurance sooner rather than later locks in a lower rate based on your current age. And choosing a term life insurance policy over a whole life option keeps the insurance costs manageable while still giving your family solid protection. To better understand how these factors are calculated read our post on how is life insurance calculated.

Cheapest Life Insurance for Smokers Over 40

Once you’re past 40 as a smoker the life insurance rates do climb. But they don’t fall off a cliff the way some people fear. Smokers over 40 who are in decent health can still qualify for life insurance at reasonable rates especially through a term life insurance policy. A 20 year term policy taken out at 42 for example still gives your family solid coverage through your peak earning years.

The key at this age is not waiting any longer. Every year you delay buying life insurance as a smoker over 40 adds to your premium and narrows your options.

Cheapest Life Insurance for Smokers Over 50

Life insurance for smokers over 50 is definitely more limited than it is for younger applicants but it’s still very much available. Term life policies with shorter terms like 10 or 15 years are the most common route. Guaranteed issue life and final expense policies also become more relevant at this age for smokers who have additional health conditions on top of tobacco use.

The honest truth is that smokers over 50 who wait even longer are going to face fewer options and higher life insurance premiums. So acting now even if the rate isn’t what you hoped is almost always the smarter move.

Cheapest Life Insurance for Smokers in the US What to Expect

Across the US life insurance rates for smokers vary based on your state’s insurance market, your age and which carrier you go with. Some states have more carriers competing which naturally drives competitive rates down. But the most important factor is still your individual health profile.

Standard life insurance underwriting means every smoker gets evaluated individually. So two 45 year old smokers can get very different life insurance quotes depending on their blood pressure, weight and medical history.

| Age Group | Term Length | Approximate Rate Range |

|---|---|---|

| 25–35 | 20 Years | Lower end of smoker rates |

| 36–45 | 20 Years | Moderate smoker rates |

| 46–55 | 15–20 Years | Higher smoker rates |

| 56–65 | 10–15 Years | Highest smoker rates |

Life Insurance for Cigar Smokers and E Cigarette or Vaping Users

Are Cigar Smokers Treated the Same as Cigarette Smokers

Not always. Life insurance cigar smoker treatment depends heavily on frequency of use. An occasional cigar smoker one or two cigars a month can sometimes qualify for life insurance at non smoker rates if there’s no detectable cotinine at the time of the life insurance medical exam. Daily cigar use on the other hand puts you squarely in the smoker classification.

So if you’re a casual cigar smoker it’s genuinely worth asking your insurance agent how different carriers handle that. Some are much more lenient than others and the difference in life insurance rates can be real.

How Insurers Handle Vaping and E Cigarette Use

E cigarette vaping life insurance is a newer category and the rules are still evolving. Right now most major life insurance companies classify vaping the same as cigarette smoking because the nicotine content is similar. Your life insurance application will ask about nicotine use broadly not just cigarettes so vaping gets captured in that question.

Some carriers are starting to differentiate between vaping and cigarette smoking but it’s still the minority. For now you should expect to be rated as a tobacco user if you vape.

Nicotine Pouches and Chewing Tobacco Where Do They Fall

Chew tobacco and nicotine pouches are both treated as tobacco use by most life insurance companies. The nicotine shows up in testing and the insurer will classify you as a smoker regardless of the delivery method. Some people assume that because they don’t actually smoke they won’t be rated as a smoker but that’s not how the life insurance application process works.

If you use tobacco in any form the insurance companies want to know about it. And their testing will confirm it.

Does Marijuana Use Affect Life Insurance for Smokers

How Life Insurance Companies View Marijuana Use

Marijuana sits in its own category for most life insurance companies and the rules vary more than with traditional tobacco use. Some insurers will rate recreational marijuana users at standard life insurance or even non smoker rates if usage is infrequent and health is otherwise good. Others treat it more like cigarette smoking and apply higher life insurance premiums.

The key factors are frequency of use, your state’s laws around marijuana and which insurance company you’re applying with. Heavy daily use tends to push life insurance rates higher regardless of carrier.

Marijuana vs Tobacco Which One Raises Your Rate More

In most cases tobacco use raises life insurance rates more predictably and more steeply than marijuana use. Life insurance companies have decades of life expectancy data on smoking and tobacco products. The data on marijuana is newer and less consistent across carriers.

So a cigarette smoker will almost always pay more than a casual marijuana user when all other factors are equal. But combine both and your smoker life insurance rates are going to reflect the cumulative health risk.

Former Smoker Life Insurance Rates What Changes After You Quit

How Long You Must Be Smoke Free Before Rates Drop

This is one of the most common questions and the answer is it depends on the carrier. Most life insurance companies require at least 12 months of being completely smoke free before they’ll consider reclassifying you. Many require 24 months. Some go as far as 5 years before offering nonsmoker rates to former smoker applicants.

The nicotine test life insurance process plays a role here too. Even if you quit smoking you may still be tested at your next policy review or if you apply for life insurance with a new carrier.

How to Request a Rate Review After Quitting Smoking

If you bought a policy as a smoker and you’ve since stopped smoking you may be able to request a rate reclassification from your insurance company. This typically involves a new life insurance medical exam to confirm there’s no nicotine in your system. If you pass and you’ve been smoke free for the required period your insurer may reclassify you at nonsmoker rates.

Not every life policy allows for this so check your contract or ask your insurance agent directly. But when it is available the quit smoking life insurance savings can be substantial.

How Much You Can Save on Life Insurance by Quitting Smoking

The quit smoking life insurance savings are real and they add up over time. Former smoker life insurance rates after reclassification can drop by 40 to 50 percent in many cases. That’s a significant reduction in life insurance premiums and it’s one of the strongest financial arguments for stop smoking efforts beyond the obvious health benefits.

Even partial progress helps. Some insurance companies offer smoker premium reduction life insurance pathways for applicants who are actively working toward quitting with documented medical support.

| Years Smoke Free | Likely Classification | Rate Impact |

|---|---|---|

| Less than 1 year | Still Smoker | No change |

| 1 to 2 years | Possible reclassification | Varies by carrier |

| 2 to 3 years | Likely eligible | Moderate reduction |

| 3 to 5 years | Strong eligibility | Significant reduction |

| 5 or more years | Non smoker rates possible | Up to 40–50% reduction |

Should You Delay Buying Life Insurance If You Are Trying to Quit Smoking

Why Waiting Is Usually the Wrong Move

Here’s the honest answer waiting to buy life insurance until after you quit smoking is a gamble that doesn’t usually pay off. Life doesn’t wait. And the longer you delay buying life insurance the older you get which means higher life insurance rates regardless of your smoking status.

If you’re actively trying to stop smoking that’s genuinely great. But apply for life insurance now as a smoker and lock in coverage while you work on quitting. You can always request a smoker premium reduction life insurance reclassification later when you’ve been smoke free long enough. Read our full post on how does life insurance work to better understand the timing of coverage.

How to Lock In Coverage Now and Renegotiate Rates Later

Buying life insurance as a smoker today doesn’t lock you into smoker life insurance rates forever. Many life insurance policies allow you to request a premium review after you’ve been smoke free for a qualifying period. So the smart move is to get covered now and plan for a reclassification down the road.

Work with an insurance agent who knows which carriers are most flexible about former smoker life insurance rates reclassification. Getting the right life policy from the start makes the renegotiation process a lot smoother when the time comes. You can also read about the life insurance underwriting process to know exactly what carriers look at when they evaluate your application.

Frequently Asked Questions

Can you get life insurance if you smoke?

Yes you can. Life insurance for smokers is widely available across the US and you won’t get turned away just for smoking. The rate will be higher than what a nonsmoker pays but coverage is absolutely there for you.

How much more do smokers pay for life insurance?

Plain and simple smokers pay roughly two to three times more than nonsmokers for the same policy. Smoker life insurance rates are higher because tobacco use shortens life expectancy and insurers price that risk into your premium.

What do life insurance companies consider “smoking”?

That’s the part most people miss. It’s not just cigarettes. Insurers count cigars chewing tobacco vaping and nicotine patches as tobacco use too. If you’ve used any nicotine product in the last 12 to 24 months you’re likely rated as a smoker.

How do life insurance companies know if I smoke?

They run a nicotine test life insurance exam that checks for cotinine in your urine or blood. And beyond that they pull your medical records and prescription history. So if you’ve been prescribed nicotine replacement products that shows up too.

What happens if I lie about smoking on my life insurance application?

Don’t do it. If the insurer finds out they can deny your death benefit and cancel your policy especially within the first two years. The tobacco user life insurance cost is worth paying honestly. Fraud on an application has real consequences.

Is life insurance more expensive for smokers?

Yes. In most cases the life insurance smoker vs nonsmoker gap is significant. But here’s the thing your overall health still matters a lot. A smoker with good blood pressure and a clean medical history will get better rates than a smoker with multiple conditions stacked together.

What is the cheapest term life insurance for smokers?

The best life insurance for smokers on a budget is usually a 20 year term policy applied for at a younger age. The earlier you lock in coverage the lower your smoker premium tends to be. Comparing quotes from multiple carriers makes a real difference too.

Can life insurance be denied for smoking?

Rarely just for smoking alone. But if tobacco use is combined with serious health conditions some carriers will decline a traditional application. Guaranteed issue policies are still available in those cases so you’re not completely without options.

9. What happens if I start smoking after I buy life insurance?

Your existing policy stays in force. The death benefit doesn’t change. But if you apply for new coverage or try to increase your policy later you’ll need to disclose your current smoking status and your rates will reflect that.

Can I get a lower rate after I quit smoking?

Yes and the quit smoking life insurance savings can be substantial. Former smoker life insurance rates after reclassification can drop by 40 to 50 percent. Most carriers require you to be smoke free for at least 12 to 24 months and then you can request a new medical exam to qualify for smoker premium reduction life insurance rates.

Your Next Step as a Smoker Looking for Life Insurance

Being a smoker doesn’t mean you can’t get life insurance as a smoker and protect the people you love. Insurance companies have options built for smokers and tobacco users at every health level and every budget. So don’t wait get life insurance today and let your coverage do the work while you focus on what matters most.

Life insurance as a smoker isn’t out of reach. It’s just about knowing where to look and what to expect. Whether you chew tobacco, vape, smoke cigars or cigarettes there are life insurance options built for you. And if you’re working toward quitting the financial reward waiting on the other side is very real.

Use our life insurance premium calculator to get a sense of your numbers. And if you want to see how different policy types compare check out our breakdown of term vs whole life insurance.

Office: 13th Analyze Street, New York, NY 10003

Phone: +1 (523) 235 0786

Email: info@lifeinsurancequotecalculator.com

Follow us on our Linkedin and Facebook!