Table of Contents

So you’ve been looking at life insurance options and someone mentioned universal life insurance. Maybe your insurance agent brought it up or you stumbled across it while comparing insurance policies online. Either way it’s one of those topics that sounds more complicated than it actually is.

Here’s the thing. A universal life insurance policy is actually one of the most flexible life insurance options out there. It gives you permanent coverage with the added ability to adjust your premium payment and death benefit over time. That’s something most other life policies simply don’t offer. If you’re still asking yourself how does life insurance work at a basic level this blog connects those dots before going deeper.

This blog breaks down exactly how it works what makes it different from whole life insurance and term life and whether it actually fits your situation. No jargon. No confusion. Just clear honest information so you can make a smart call for your family.

What Is Universal Life Insurance?

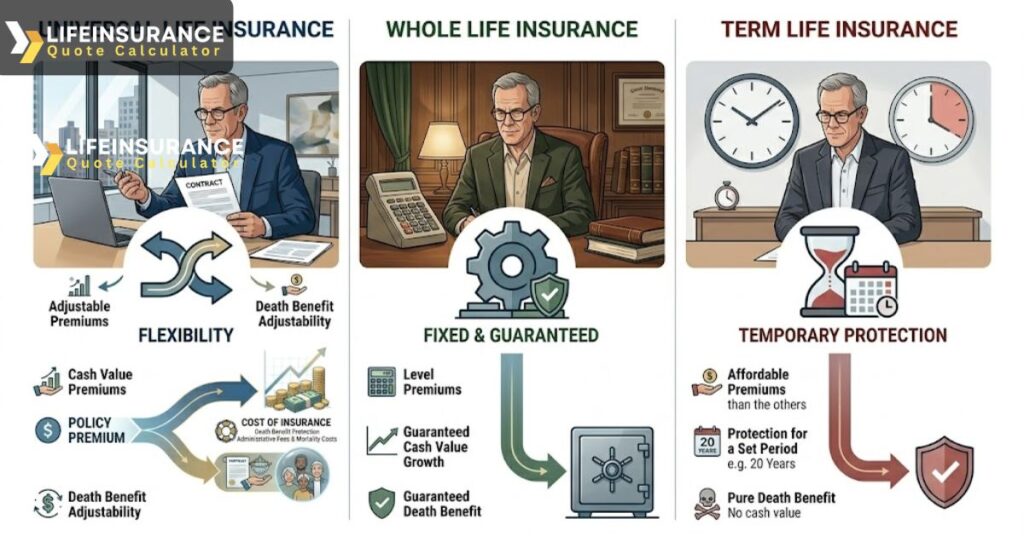

Universal life insurance is a type of permanent life insurance that keeps you covered for your entire life as long as your premium payment keeps the policy going. Unlike term life insurance which only covers you for a set number of years a universal life insurance policy stays active indefinitely.

But what really sets it apart is the built in flexibility. Most permanent life insurance products lock you into fixed payments. A universal life insurance policy lets you adjust both your premium and your death benefit depending on where you are in life. That kind of control matters especially when your income or family situation changes. To get a proper picture of how life insurance is calculated it helps to know which type of policy you’re looking at first.

How a Universal Life Insurance Policy Works

When you pay your life insurance premium into a UL policy the insurance company splits that payment into two parts. One part covers the actual cost of insurance which is what keeps your death benefit active and the other part goes into a cash value account that grows over time.

The cash value earns interest credited by the life insurance company at a rate that varies depending on the type of universal life insurance you hold. Over time that policy’s cash value builds up and becomes something you can actually use while you’re still alive.

The Two Parts of Every Universal Life Premium Payment

Every single premium payment you make gets divided. Plain and simple.

The first part pays the cost of insurance which covers the life insurance coverage itself and any policy charges the issuing insurance company applies. The second part goes directly into your cash value account where it starts to grow based on how the policy is structured.

And here’s what most people miss. If your cash value grows enough over time you can actually use that cash value to pay your premium directly. That means in certain situations your policy can sustain itself without you writing a check every month.

| Part of Premium | What It Does | Where It Goes |

|---|---|---|

| Cost of Insurance | Keeps your death benefit active and covers policy charges | Paid to the insurance company as protection cost |

| Cash Value Contribution | Builds your savings component inside the policy | Goes into your cash value account to grow over time |

Types of Universal Life Insurance Policies

Not all universal life insurance policies are built the same way. There are a few different versions and each one works differently depending on how the cash value growth happens inside the policy.

Guaranteed Universal Life Insurance

Guaranteed universal life insurance is the most straightforward version. It focuses more on keeping the death benefit solid and permanent rather than building a big cash value. The premiums are lower than traditional whole life insurance and the policy is designed to stay active as long as you keep making payments. It’s a solid pick for people who want lifelong coverage without the higher cost of whole life policies.

Indexed Universal Life Insurance (IUL Life Insurance)

Indexed universal life insurance ties your cash value growth to a stock market index like the S&P 500. But here’s what makes it different from actually investing in the market. Your money isn’t directly in mutual funds or stocks. Instead the insurance company credits interest based on how that index performs with a floor that usually protects you from losing money in a bad year. IUL life insurance appeals to people who want more growth potential than a standard UL policy but don’t want the full risk of market exposure.

Variable Universal Life Insurance

Variable universal life insurance takes things a step further. With this type your cash value is invested directly into investment options like mutual funds called sub accounts. That means the value of the policy can grow faster but it can also drop if the market performs poorly. This is the highest risk version of universal life insurance and it suits people who are comfortable with market fluctuation and want maximum growth potential inside a permanent life insurance policy.

Survivorship Universal Life Insurance

Survivorship universal life covers two people typically a married couple under a single life insurance policy. The death benefit pays out after both insured individuals pass away rather than after the first one. It’s often used for estate planning and can be a smart way to leave a legacy for children or future generations.

| Type | Premiums | Cash Value Growth | Risk Level | Best For |

|---|---|---|---|---|

| Guaranteed ULI | Fixed and lower | Minimal | Low | Lifelong death benefit focus |

| Indexed ULI (IUL) | Flexible | Index linked with floor | Medium | Growth potential with protection |

| Variable ULI | Flexible | Market based sub accounts | High | Maximum growth potential |

| Survivorship ULI | Flexible | Varies by structure | Medium | Estate planning for couples |

How Does Universal Life Insurance Cash Value Work?

The universal life insurance cash value is one of the biggest reasons people choose this type of permanent life insurance policy over simpler options. It’s real money that grows inside your policy and it belongs to you.

How Cash Value Builds Inside a Universal Life Policy

Every time you make a premium payment a portion of it flows into your cash value account. From there the insurance company credits interest based on your policy type. The cash value growth is tax deferred which means you don’t pay taxes on the gains while they sit inside the policy. Over time that compounding effect can build a meaningful amount of money inside your policy. You can also check out our breakdown of life insurance tax benefits to see exactly how these tax advantages apply to your situation.

What You Can Do With the Cash Value of Your Universal Life Insurance

Once your policy’s cash value reaches a certain level you’ve got real options. You can take a withdrawal directly from the cash value of the policy. You can take out a policy loan against it. Or in some cases you can use that cash value to pay your ongoing premium payment so the policy remains in force without coming out of pocket. These options give the policy owner real financial flexibility that a term policy or basic term life coverage simply can’t match.

Can You Borrow From a Universal Life Insurance Policy?

Yes and this is one of the most useful features of universal life insurance. A policy loan lets you borrow against the cash value of the policy without a credit check and without a fixed repayment schedule. The life insurance company charges interest on the loan but the money doesn’t get reported as income so it stays tax friendly. The one thing to watch is that if your policy loan balance gets too large and eats into the cash value your policy lapses.

Can You Cash Out a Universal Life Insurance Policy?

You can surrender the policy and receive the remaining cash value after any policy charges and outstanding policy loan balances are subtracted. But cashing out ends your coverage completely. A withdrawal is a softer option. You take out a portion of the cash value without fully surrendering the policy though large withdrawals will reduce your death benefit and can affect the policy’s cash value going forward.

| Cash Value Option | How It Works | Things to Know |

|---|---|---|

| Policy Loan | Borrow against cash value without a credit check | Interest accrues. Large loans can cause policy lapse if not managed |

| Withdrawal | Take out a portion of cash value directly | Reduces death benefit. May have tax implications above cost basis |

| Premium Payment | Use cash value to cover your premium | Keeps policy in force without out of pocket payment |

| Full Surrender | Cash out the entire policy value | Coverage ends permanently. Surrender charges may apply |

Universal Life Insurance vs Whole Life: Differences

People mix these two up constantly. Both are permanent life insurance options and both build cash value but they work very differently. Whole life insurance has fixed premiums and a guaranteed cash value growth rate. Universal life and whole life both offer lifelong coverage but a universal life insurance policy gives the policy owner control over the flexible premium and adjustable death benefit. For a full side by side breakdown read our detailed post on term vs whole life insurance which covers how these permanent options stack up against each other.

Which Is Better — Universal or Whole Life Insurance?

That honestly depends on what you need. If you want guaranteed predictable growth and you don’t want to think about managing your policy then whole life insurance might suit you better. But if your income fluctuates or your coverage needs are likely to shift over the years a universal life insurance policy gives you room to breathe. Universal life vs whole life really comes down to control versus certainty.

| Feature | Universal Life | Whole Life |

|---|---|---|

| Premiums | Flexible and adjustable | Fixed for life |

| Death Benefit | Adjustable within limits | Fixed and guaranteed |

| Cash Value Growth | Varies by policy type | Guaranteed fixed rate |

| Policy Management | Requires periodic review | Runs on autopilot |

| Cost | Generally lower than whole life | Higher fixed premiums |

| Dividends | Not typically offered | Available with participating policies |

Universal Life Insurance vs Term Life Insurance

Term life insurance is the simpler more affordable option. You pick a term usually 10 20 or 30 years and pay your life insurance premium and your beneficiary gets the death benefit if you pass during that period. When the term policy ends the coverage is gone. Universal life insurance costs more but it doesn’t expire. And while a term life policy has no cash value whatsoever a universal life insurance policy is building something real on the side the whole time.

When Term Life Makes More Sense Than a Universal Life Policy

If you’re young and your main goal is protecting your family’s income during your working years term life insurance is a practical and cost effective answer. It gives you solid life insurance coverage during the years your family needs it most without the higher premium that comes with permanent life insurance. Use our term life insurance calculator to quickly see what that coverage looks like for your age and health profile.

When Universal Life Insurance Is the Better Fit

When you want coverage that doesn’t expire the ability to build cash value over time and the flexibility to adjust your premium payment and adjustable death benefit as life changes then a universal life insurance policy starts making a lot of sense. It’s particularly useful for estate planning business purposes or when you’ve maxed out other life insurance options and want an additional financial tool.

| Feature | Universal Life | Term Life |

|---|---|---|

| Coverage Duration | Permanent (lifetime) | Fixed term (10/20/30 years) |

| Cash Value | Yes — builds over time | No cash value |

| Premium Flexibility | Adjustable within limits | Fixed for the term |

| Death Benefit | Adjustable | Fixed amount |

| Premium Cost | Higher | Lower |

| Best For | Lifelong coverage and cash building | Affordable income replacement |

Flexible Premium Life Insurance: How Premiums Work in a Universal Life Policy

One of the standout features of universal life insurance is that the premium isn’t locked in. You have a minimum premium that keeps the policy alive and a maximum based on IRS limits for permanent life insurance policy funding. Anywhere in between is fair game. So if you have a good year financially you can put more into the cash value. If things get tight you can drop down to the minimum premium payment and keep your policy remains in force.

What Happens If You Miss a Premium Payment?

Missing a premium payment doesn’t automatically kill your universal life insurance policy. The insurance company will draw from your cash value to cover the cost of insurance and policy charges if your account has enough in it. So the life insurance policy keeps going even if you skip a month. But if the cash value runs dry and you’re not making premium payments the policy lapses and you lose your life coverage. The life insurance underwriting process determines how your policy is structured from day one so understanding it can help you avoid these situations.

Why Did My Universal Life Insurance Premium Change?

The cost of insurance inside your UL policy goes up as you get older because the underwrite risk to the life insurance company increases with age. So even if you’re paying the same dollar amount each month a bigger chunk of that payment is going toward the cost of insurance and less is going into your cash value. If your cash value hasn’t been growing well you might need to increase your premium payment to keep the policy active.

Universal Life Insurance Option A vs Option B — Death Benefit Explained

When you set up a universal life insurance policy you’ll typically choose between two death benefit structures. Option A keeps your total death benefit fixed. As your cash value grows it starts to replace part of the pure death benefit inside the policy which helps keep your cost of insurance lower over time. Option B is the increasing death benefit. Your beneficiary receives the base death benefit plus the full cash value of the policy at the time of your passing.

| Feature | Option A (Level Death Benefit) | Option B (Increasing Death Benefit) |

|---|---|---|

| Death Benefit Structure | Fixed total payout | Base benefit plus full cash value |

| Cash Value Impact | Replaces part of pure insurance over time | Added on top of base death benefit |

| Cost of Insurance | Lower — risk covered decreases over time | Higher — insurance company covers more risk |

| Best For | Lower ongoing cost and estate efficiency | Maximum payout growth for beneficiary |

Universal Life Insurance Pros and Cons

Like any life insurance policy a UL policy has real strengths and real limitations. Here’s an honest look at both sides.

Pros of Universal Life Insurance Policies

The flexible premium structure is a genuine advantage for people whose income isn’t perfectly consistent. The adjustable death benefit means you can scale your life coverage up or down as your family’s needs shift. The cash value growth is tax deferred and gives you access to loans or withdrawals without going through a bank. And the policy stays active for life so your beneficiary doesn’t have to worry about the coverage expiring.

What Are the Disadvantages of Universal Life Insurance?

The truth is universal life insurance requires more attention than a simple whole life insurance policy or term life plan. The cost of insurance rises as you age and if your cash value doesn’t keep up your policy can be at risk. The flexible premium is a great feature but it can also lead to underfunding if you consistently pay the minimum without checking your policy illustration. Variable universal life insurance adds market risk on top of that. And indexed universal life insurance has caps that limit your upside even in strong market years.

| Pros | Cons |

|---|---|

| Flexible premium payments | Requires active policy management |

| Adjustable death benefit | Cost of insurance rises with age |

| Tax deferred cash value growth | Underfunding can cause policy lapse |

| Lifetime coverage | More complex than term life |

| Access to loans and withdrawals | Variable type carries market risk |

| Useful for estate planning | IUL caps limit upside in strong years |

Is Universal Life Insurance Right for You?

If you want permanent life insurance that gives you flexibility over both your premium payment and your death benefit and you’re comfortable checking in on your policy occasionally then universal life insurance is worth a serious look. If you prefer something that runs completely on autopilot whole life insurance or even a long level term policy might suit you better.

Checklist — Who Should Consider a Universal Life Insurance Policy

A universal life insurance policy tends to work well for people who want lifelong life coverage but need adjustable payment flexibility. It also suits people interested in building cash value over time that they can access through a policy loan or withdrawal. Business owners using life insurance products for buy sell agreements often choose universal life policies for exactly this reason. And those thinking about estate planning often find survivorship universal life to be a smart fit within a broader financial plan.

Universal Life Insurance Rates — What Affects Your Premium

Your universal life insurance rates are shaped by several factors. Age at the time you apply matters a lot. Younger applicants get lower cost of insurance rates. Your health status plays a big role too since the insurance company uses it to underwrite your policy. Smoking status lifestyle and the amount of death benefit you choose all feed into your final life insurance premium. The type of universal life insurance you select whether that’s guaranteed universal life or indexed universal life insurance also affects your rate. People with certain health conditions like diabetes or high blood pressure can still qualify though the rate tier may differ.

Tax Implications of Universal Life Insurance

The cash value inside your universal life insurance policy grows tax deferred. That means you’re not paying taxes on the gains each year as they accumulate. Policy loan proceeds are generally not considered taxable income as long as the policy remains in force. And the death benefit paid to your beneficiary is typically income tax free. That combination makes universal life insurance a useful tool when thinking about tax efficient wealth transfer. Read our full post on life insurance tax benefits for a deeper look at these advantages.

Can Universal Life Insurance Help With Estate Planning?

It absolutely can. The death benefit passes directly to your beneficiary outside of probate which means it moves quickly and privately. Survivorship universal life is especially popular in estate planning because it covers two lives and pays out when it’s most needed for the surviving heirs. When structured correctly a universal life insurance policy can help cover estate taxes preserve generational wealth and create a financial legacy.

Best Universal Life Insurance — What to Look for Before You Buy

Choosing the best universal life insurance isn’t just about the lowest premium. You want to look at the financial strength of the life insurance company how transparent the policy illustration is how the cash value growth is structured and what policy options are available to you if your needs change. Work with a licensed insurance agent who can show you a clear policy illustration that projects the value of the policy over time under different scenarios.

IUL vs Whole Life — Which Builds More Cash Value Over Time?

IUL vs whole life is a real debate in the life insurance world. Indexed universal life insurance has the potential to build cash value faster in strong market years because of the index linked crediting. But whole life insurance offers guaranteed cash value growth that doesn’t depend on market performance at all. For some people the certainty of whole life policies is worth more than the higher potential growth of IUL life insurance.

IUL Life Insurance — How Indexed Universal Life Differs From Standard ULI

In a standard UL policy your cash value earns a declared interest rate set by the insurance company. It’s stable and predictable. Indexed universal life insurance replaces that declared rate with a crediting method tied to an index. The result is that IUL life insurance tends to offer higher growth potential than standard universal life insurance in good years and still protects your cash value from negative returns in bad ones.

| Feature | IUL (Indexed ULI) | Whole Life | Standard ULI |

|---|---|---|---|

| Cash Value Growth | Index linked with floor and cap | Guaranteed fixed rate | Declared interest rate |

| Market Risk | Medium | None | Low |

| Premium Flexibility | Flexible | Fixed | Flexible |

| Downside Protection | Yes — floor prevents losses | Yes — guaranteed | Declared rate varies |

| Growth Potential | Higher in good years | Steady and predictable | Moderate |

| Best For | Growth with protection | Certainty and simplicity | Basic flexible coverage |

Universal Life Insurance Calculator — Get a Free Instant Quote

One of the best ways to see how universal life insurance fits your situation is to run the numbers yourself. A universal life insurance calculator lets you plug in your age health status and desired death benefit to see what your life insurance premium might look like and how your cash value could grow over time.

How to Use the Life Insurance Quote Calculator to Get a Universal Life Insurance Quote

At Life Insurance Quote Calculator you can get a real estimate without giving your phone number or sitting through a sales call. You enter a few basic details about yourself and the tool pulls together a realistic picture of what your universal life insurance coverage could look like. It pulls from real life insurance company pricing models so the numbers you see are grounded in actual universal life insurance rates.

You can also use the life insurance premium calculator to compare how different types of universal life insurance stack up against each other and against term life insurance side by side.

Get a Universal Life Insurance Quote in Under 2 Minutes

Getting a universal life insurance quote doesn’t have to be a long drawn out process. Use the term life insurance calculator to start comparing life insurance options right now. In most cases you’ll have a clear picture of your premium range and death benefit options in under two minutes. No credit check. No phone call. Just your number ready to work with.

Frequently Asked Questions

1. What is universal life insurance and how does it work

Universal life insurance is a type of permanent life insurance that gives you lifelong coverage with flexible payments. It builds cash value over time and you can adjust your premium or death benefit based on your needs. I have seen many people like it because it gives more control than term life.

2. What are the disadvantages of universal life insurance

The downside is cost and complexity. If you do not manage payments well the policy can lapse and fees can eat into the cash value. In some cases returns are not as strong as expected which surprises people.

3. Is universal life insurance a good investment

It can work as a long term plan but it is not always the best pure investment. Some use indexed universal life insurance or variable universal life insurance for growth but results depend on market conditions. So it really depends on your goal.

4. How much does universal life insurance cost

Cost varies based on age health and coverage amount. Universal life insurance rates are usually higher than term life but flexible premium life insurance lets you adjust payments. I have noticed younger buyers get better pricing.

5. Does universal life insurance build cash value

Yes it builds cash value over time. The policy earns interest or follows an index in IUL life insurance. This cash value can be used later through withdrawals or loans which many policy owners find useful.

6. Can universal life insurance lapse

Yes it can lapse if there is not enough cash value or if premiums are not paid. This is common when people lower payments too much. Keeping track of policy performance helps avoid this issue.

7. Does universal life insurance have flexible premiums

Yes flexible premiums are a key feature. You can increase or decrease payments depending on your financial situation. But paying too little for too long can affect the policy stability.

8. Is universal life insurance permanent or term

It is permanent life insurance. Unlike term life it does not expire as long as the policy stays funded. Guaranteed universal life insurance is designed to keep coverage stable.

9. What is the difference between universal life insurance and whole life insurance

Universal life vs whole life comes down to flexibility. Whole life has fixed premiums and guaranteed growth. Universal life offers adjustable payments and variable cash value growth which gives more control.

10. Who should buy universal life insurance

It suits people who want long term coverage with flexibility. Business owners or high income earners often choose it for planning and cash value growth. But it is not ideal for someone looking for simple low cost coverage.

Universal Life Insurance: Final Thoughts Before You Decide

Universal life insurance gives you flexibility, lifelong coverage, and the ability to build cash value over time. It works best when you actively manage the policy and understand how premiums and costs interact. If you want control and long-term financial planning in one place, this policy can be a powerful option.

Office: 13th Analyze Street, New York, NY 10003

Phone: +1 (523) 235 0786

Email: info@lifeinsurancequotecalculator.com

Follow us on our Linkedin and Facebook!