Table of Contents

Picking the right life insurance company is one of the most personal financial decisions you will ever make. And in 2026, the market is packed with options. That is actually a good thing because it means there is a real life insurance policy out there for just about every family in the United States. But more options also means more confusion.

So here is what this blog does. It breaks down the best life insurance companies 2026 by what they are actually best at. Whether you want term life insurance, whole life insurance, universal life coverage or a plan with no medical exam required, you will find a clear answer here.

Before you even start comparing plans, use the Life Insurance Quote Calculator to get a real number based on your age, health and budget.

What Makes a Life Insurance Company the Best in 2026?

Not every life insurer is built the same. Two companies can offer the exact same coverage amount and the monthly cost can be 30 percent apart. So before you look at any list of life insurance companies, it helps to understand what you are actually comparing.

AM Best Ratings and Financial Strength Explained

The AM Best rating tells you how financially strong a life insurance company is. Think of it like a credit score for insurers. An A++ or A+ rating means the company has the financial muscle to pay out claims even during rough economic periods. An A rating is still solid. Anything below B++ and you should pause before signing anything.

The national association of insurance commissioners also keeps public records of complaint ratios for every carrier operating in the U.S. A low complaint index means fewer customers had issues with claims or billing. Both the AM Best grade and the complaint index together give you a real picture of what a company is actually like to work with.

| AM Best Rating | What It Means | Is It Safe to Buy? |

| A++ | Superior financial strength | Yes — top tier |

| A+ | Superior | Yes — excellent choice |

| A | Excellent | Yes — very reliable |

| A- | Excellent with minor concerns | Yes — still strong |

| B++ | Good | Caution — research further |

| B+ | Good with limitations | Caution — compare carefully |

What Life Insurance Company Reviews Actually Tell You

Reviews from real customers can save you a lot of headaches. But you have to read them with some context. Most people only leave a review after a claim. So when you see a lot of negative reviews about the claims process, that is a real warning sign. On the other hand, companies with high ratings for customer service and fast payouts are the ones worth shortlisting.

When you compare life insurance companies, look past the monthly premium alone. The life insurance company reviews that matter most are about what happens when a family actually needs the money. That is the moment the whole thing is designed for.

Key Factors to Compare Before Choosing a Company

Here is what actually moves the needle when you are shopping for life insurance. Financial rating comes first. Then look at the types of life insurance policies the company offers since some carriers only specialize in term life policies and do not offer good permanent life insurance options. Also check whether the company allows you to get life insurance quotes online without talking to an insurance agent first.

| Factor | Why It Matters | What to Look For |

| AM Best Rating | Proves financial stability | A- or better |

| Claim Payout Rate | Shows reliability when it counts | 95% or higher |

| Policy Types Available | Matches your actual need | Term, whole, universal |

| No-Exam Option | Faster approval process | Available for healthy applicants |

| Online Quote Access | Saves time without pressure | Instant quote tool available |

| Rider Options | Customizes your coverage | Critical illness, waiver of premium |

Best Life Insurance Companies 2026 — What to Look for in Each Category

These picks are based on life insurance company ratings, coverage flexibility, premium affordability and real customer feedback across the U.S. market. This is not a ranking where one company wins for everyone. It is more like a match system where the right pick depends on what you actually need.

Best Overall Life Insurance Company 2026

For most American families, the best life insurance company is one that balances price, reliability and flexibility. The strongest overall options offer term life insurance policies at highly competitive rates with solid underwriting for people with minor health conditions. Look for carriers sitting at an A+ AM Best rating with a clean online application process.

That said, if you want to compare life insurance before making any call, the Term Life Insurance Calculator lets you plug in your details and see real numbers right away.

Best Term Life Insurance Company 2026

The best carriers for term life insurance rates are the ones that consistently price low for healthy non-smoking applicants. They offer level term life insurance across 10, 20 and 30-year terms and the application process can be completed completely online. For anyone asking how much life insurance they can get for under $25 a month, affordable term life insurance from a well-rated carrier is almost always the first answer.

Just make sure you are comparing the full life insurance cost including any riders you add on. A rider that adds $8 per month can be worth it or unnecessary depending on your situation.

Best Whole Life Insurance in 2026

The best whole life insurance policy options come from carriers with decades of financial stability behind them. Longevity in the insurance industry means something real. Their whole life policies build guaranteed cash value over time and the death benefit is locked in for life. Some carriers also pay dividends to policyholders which can be used to reduce premiums or grow the cash value further.

The whole life policies tend to run higher than term insurance on a monthly basis. But the lifelong coverage and cash accumulation make it a different product entirely and the right fit for families focused on long-term estate planning.

Best for Low Rates and Cheap Premiums

Among the cheapest life insurance companies in the U.S. right now the best value comes from carriers offering a wide life insurance coverage range from $50,000 all the way up to several million dollars. That flexibility means you are not forced into a fixed benefit amount. Their rates for healthy applicants in their 30s are genuinely among the most affordable term life insurance prices you will find in the current market.

Best for Seniors in 2026

Seniors shopping for life insurance in 2026 have more life insurance options than most people think. The strongest carriers for older applicants offer products specifically designed with seniors in mind. Guaranteed issue whole life insurance is available without a health review for coverage up to certain limits. The premiums are higher than term life policies but the guaranteed issue option removes the barrier of a full health review which is a real advantage for seniors with existing health conditions.

Best for No-Medical-Exam Policies

Not everyone wants to schedule a paramedical exam to get life insurance. Several strong U.S. carriers have made no-exam life insurance a real and affordable option with instant online decisions for qualifying applicants. Life insurance without a medical exam does tend to cost slightly more. But for healthy applicants in their 30s and 40s the price difference is often minimal and the time saved makes it worth considering.

Best for Converting to Permanent Life Insurance

The best carriers for conversion are the ones whose term life insurance policies include strong conversion options that let you move into a permanent life insurance policy later without going through underwriting again. That means if your health changes after you buy life insurance on a term plan you still have a clear path to lifelong coverage. For families planning ahead for estate needs this flexibility matters a lot more than most buyers realize upfront.

Best for Business Owners

Some life insurance providers build life insurance products with business applications specifically in mind. Key person coverage, buy-sell agreements and executive benefit plans are all areas where specialized carriers have real experience. Their individual life insurance policies can also be structured for business use and the life insurance policy can help protect a company from the financial impact of losing a critical team member.

Best Term Life Insurance Companies 2026 — Consumer Reports Style Breakdown

When people search for the best term life insurance companies consumer reports style, what they really want is a simple honest comparison without the sales pitch. So here it is.

What Separates the Best Term Life Insurance Companies From the Rest

The best term life insurance companies do a few things really well. They price fairly for your actual health profile instead of giving everyone the same rate. They offer flexible term length options across 10, 20 and 30-year windows. And they make it easy to buy life insurance without having to sit through a long phone call with an insurance agent.

Beyond price the best carriers also offer clear answers about what happens when the term life insurance ends. Can you renew? Can you convert to permanent life insurance? Those answers matter a lot more than most buyers realize upfront. A term life insurance policy that comes with a solid conversion option is worth slightly more per month in most cases.

How to Read a Term Life Insurance Rate Comparison

When you compare life insurance quotes across carriers for the same applicant profile the price difference can be 20 to 30 percent. That gap exists because every carrier weights health and lifestyle risk factors slightly differently in their underwriting models.

This is exactly why getting life insurance quotes from multiple carriers is so important. Going direct to a single carrier and accepting their first number is almost always more expensive than using a life insurance quote calculator that pulls from the full market. The best term life insurance rate for your profile is almost never the first number you see.

Cheapest Life Insurance Companies 2026 — Lowest Rates by Profile

Price is not everything in life insurance but it matters. Here is a breakdown of what the cheapest life insurance companies actually offer by specific applicant profile so you can find what is genuinely affordable for your situation.

Cheapest Life Insurance for Women in 2026

Women pay less for life insurance than men across almost every age group. This comes down to life expectancy data. Women in the U.S. tend to live longer and that lower mortality risk means lower premiums from most carriers. At age 30 a healthy non-smoking woman can get a $500,000 level term life insurance policy for around $16 to $18 per month on a 20-year term. That is one of the best value points in all of life insurance coverage anywhere in the U.S. market right now.

| Age | Monthly Rate (Female Non-Smoker, $500K, 20-Year Term) |

| 25 | ~$11/mo |

| 30 | ~$16/mo |

| 35 | ~$22/mo |

| 40 | ~$36/mo |

| 45 | ~$58/mo |

Cheapest Life Insurance for Men in 2026

Men pay higher life insurance rates on average because of shorter average life expectancy in the U.S. Still a healthy non-smoking 35-year-old male can lock in $500,000 of term life insurance coverage for around $28 to $32 per month depending on the carrier and the term length chosen. Buying early is the single biggest factor in keeping the cost of life insurance low for men. Every year you wait adds roughly 8 to 10 percent to your premium.

| Age | Monthly Rate (Male Non-Smoker, $500K, 20-Year Term) |

| 25 | ~$14/mo |

| 30 | ~$23/mo |

| 35 | ~$29/mo |

| 40 | ~$47/mo |

| 45 | ~$77/mo |

Cheapest Life Insurance for Seniors in 2026

Seniors have a narrower set of life insurance options but those options have genuinely improved in recent years. Guaranteed issue whole life insurance is available without a health review for applicants up to age 80 in most states. The coverage amounts are lower typically capped at $25,000 to $50,000 and the premiums are higher relative to the benefit. But for seniors focused on final expense coverage it removes the medical barrier entirely and provides real peace of mind.

Cheapest Life Insurance for Smokers in 2026

Smoking is the single biggest rate driver in the insurance industry outside of age. A smoker at age 40 can pay nearly three times what a non-smoker pays for identical life insurance coverage. The good news is that most life insurance companies reclassify you as a non-smoker after 12 consecutive months of tobacco-free living. Quitting and waiting that year before you purchase a life insurance policy can cut the cost of term life insurance by 40 to 60 percent. That is one of the highest-impact moves any tobacco user can make before applying.

| Age | Non-Smoker Rate | Smoker Rate | Annual Difference |

| 30 | ~$23/mo | ~$68/mo | ~$540/yr more |

| 35 | ~$29/mo | ~$89/mo | ~$720/yr more |

| 40 | ~$47/mo | ~$134/mo | ~$1,044/yr more |

| 45 | ~$77/mo | ~$218/mo | ~$1,692/yr more |

Types of Life Insurance You Need to Know About in 2026

There is no single type of life insurance policy that works for every person. The right choice depends on your age, your budget, how long you need coverage and whether you want life insurance to also build cash value over time. Here is a plain-English breakdown of each type of life insurance available to U.S. families in 2026.

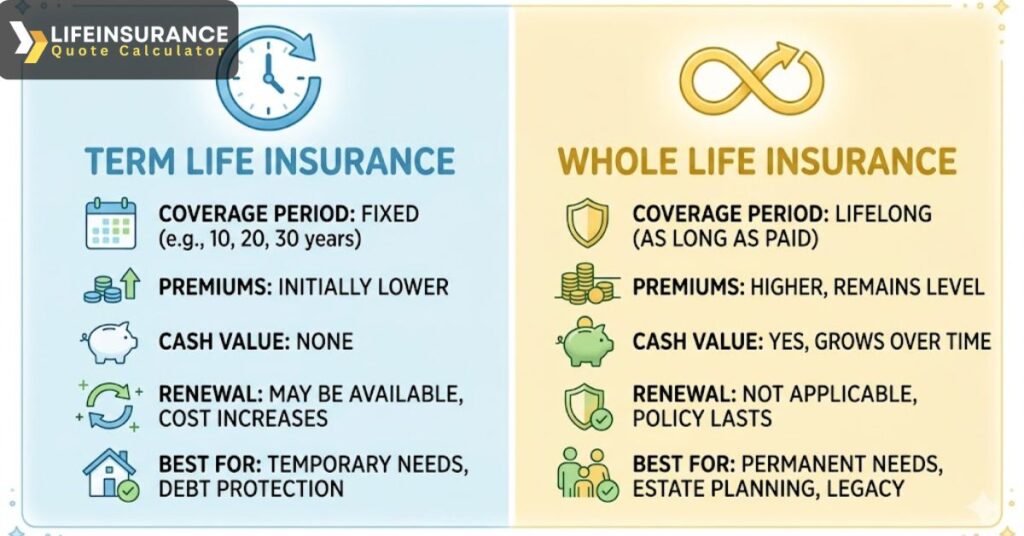

Term Life Insurance — The Most Affordable Option

Term life insurance is exactly what the name says. You pick a term length and pay a fixed monthly rate for that period. If you pass away during the term your beneficiaries get the death benefit. If the term ends and you are still alive the coverage stops.

It is the most popular type of life insurance in the U.S. because it gives families the most coverage for the lowest cost. Affordable term life insurance starts as low as $14 per month for a healthy 25-year-old getting $500,000 in coverage. Most term life policies run for 10, 20 or 30 years and you can often get life insurance quotes and buy life insurance completely online without ever speaking to an agent. That kind of access is what makes term life insurance online so popular for first-time buyers.

Whole Life Insurance — Lifetime Coverage With Cash Value

Whole life insurance covers you for your entire life as long as premiums are paid. Unlike term it also builds a guaranteed cash value over time that you can borrow against. The whole life insurance policy premium is fixed and will never increase which is a real comfort for long-term planning.

The trade-off is cost. Whole life policies cost significantly more per month than term life insurance policies for the same death benefit. But if you need life insurance to cover estate taxes, final expenses or want to leave a guaranteed inheritance, whole life insurance is built exactly for that purpose.

Universal Life Insurance — Flexible Premiums and Death Benefits

Universal life insurance is a form of permanent life insurance that allows you to adjust your premiums and death benefit over time within certain limits. Universal life policies also build cash value but the growth is tied to current interest rates rather than a fixed schedule like whole life policies.

There is also variable life insurance and variable universal life insurance where the cash value is invested in market-based sub-accounts. These carry more risk but also more growth potential. For most families comparing whole or universal life comes down to how much flexibility they want in their premiums and how comfortable they are with investment risk. Whole and universal life insurance both offer lifelong protection. The difference is really in how the cash value grows and how much control you want over your premium payments.

| Policy Type | Coverage Duration | Cash Value? | Best For | Avg Monthly Cost |

| Term Life | 10-30 years | No | Income replacement | ~$14-$50/mo |

| Whole Life | Lifetime | Yes (guaranteed) | Estate planning/final expense | ~$150-$400/mo |

| Universal Life | Lifetime (flexible) | Yes (interest-based) | Flexible premium payers | ~$100-$350/mo |

| Variable Universal Life | Lifetime | Yes (market-based) | Growth-focused buyers | ~$150-$500/mo |

How Much Does Life Insurance Cost in 2026?

The cost of life insurance depends on several personal factors and it varies more than most people expect. Age, gender, health class and whether you smoke are the four biggest pricing variables. Here is what real 2026 rates look like across different applicant profiles in the U.S.

Average Life Insurance Rates by Age and Gender

Here is what life insurance rates look like for a healthy non-smoking applicant getting $500,000 in term life insurance coverage on a 20-year term. These reflect current 2026 market pricing across U.S. carriers.

| Age | Male Monthly Rate | Female Monthly Rate |

| 25 | ~$20/mo | ~$16/mo |

| 30 | ~$23/mo | ~$18/mo |

| 35 | ~$29/mo | ~$22/mo |

| 40 | ~$47/mo | ~$36/mo |

| 45 | ~$77/mo | ~$58/mo |

| 50 | ~$127/mo | ~$96/mo |

Nonsmoker vs. Smoker Life Insurance Rates Compared

One of the most common questions people have is how much smoking actually affects the cost of a life insurance policy. The answer is quite a lot. Smokers are placed in a higher risk class and pay substantially more than non-smokers of the same age and health status for identical life insurance coverage. The gap between smoker and non-smoker rates is widest at older ages and it only grows with time.

| Age | Nonsmoker Rate | Smoker Rate | Annual Difference |

| 30 | ~$23/mo | ~$68/mo | +$540/yr |

| 35 | ~$29/mo | ~$89/mo | +$720/yr |

| 40 | ~$47/mo | ~$134/mo | +$1,044/yr |

| 45 | ~$77/mo | ~$218/mo | +$1,692/yr |

How Your Health Class Affects What You Pay

Every carrier assigns applicants to a health class during underwriting and that class directly determines your rate. Getting placed in Preferred Plus versus Standard can mean a difference of $20 to $40 per month on a $500,000 term life insurance policy. Only about 10 to 15 percent of applicants qualify for Preferred Plus so most people land in Preferred or Standard. That is completely normal and nothing to worry about.

| Health Class | Description | Monthly Rate ($500K, 20-Year, Male 35) |

| Preferred Plus | Best possible health | ~$24/mo |

| Preferred | Very good health, minor issues | ~$29/mo |

| Standard Plus | Average health, some conditions | ~$36/mo |

| Standard | Managed health conditions | ~$44/mo |

| Table Rating | Higher risk applicants | ~$58+/mo |

How Much Life Insurance Do You Actually Need?

Most people guess at this number. But the life insurance amount you choose should be based on real math not a gut feeling. Here are the two most commonly used methods that financial professionals rely on across the U.S.

The DIME Method — Debt, Income, Mortgage, Education

DIME stands for Debt, Income, Mortgage and Education. Start by adding up your total outstanding debts outside of your mortgage. Then calculate how many years of income your family would need to stay financially stable. Add the full remaining balance on your mortgage. Then add up the projected education costs for each child. That total becomes your minimum life insurance coverage target.

The DIME method gives you the most detailed picture of how much life insurance you need and it accounts for costs that the simpler income multiplier misses. Things like student loans, credit card balances and childcare costs all factor in here.

| DIME Component | What to Include | Example Amount |

| Debt (D) | Car loans, credit cards, student loans | $40,000 |

| Income (I) | Annual income x years needed | $75,000 x 10 = $750,000 |

| Mortgage (M) | Full remaining home loan balance | $280,000 |

| Education (E) | College costs per child | $120,000 |

| Total Coverage Target | $1,190,000 |

The Income Multiplier Method — A Quick Starting Point

If the DIME method feels like too much math right now the income multiplier is a fast and reasonable starting point. Simply multiply your annual income by 10. If you earn $60,000 a year you should aim for at least $600,000 in life insurance coverage. This gives your family time to adjust financially without your income and it is the most widely used rule of thumb in the U.S. insurance industry.

| Annual Income | x10 Coverage Estimate | Suggested Range |

| $40,000 | $400,000 | $400K-$600K |

| $60,000 | $600,000 | $600K-$900K |

| $80,000 | $800,000 | $800K-$1.2M |

| $100,000 | $1,000,000 | $1M-$1.5M |

Which Method Works Best for Your Situation

For most families with young children and a mortgage, the DIME method gives a more accurate number. The income multiplier is a floor not a ceiling. If you have significant debts or education costs to plan for, DIME will get you closer to the life insurance amount that actually protects your family the way it is supposed to. Either way both methods point to the same next step: use a life insurance calculator to see what your real monthly cost would be at that coverage level.

How to Save on Life Insurance Rates in 2026

Getting the right coverage at a fair price is completely possible if you approach it the right way. Here are the five moves that consistently make the biggest difference on life insurance rates for U.S. applicants.

Buy a Policy While You Are Young

Age is the most powerful pricing variable in life insurance. Rates increase roughly 8 to 10 percent for every year you delay. A 30-year-old buying a 20-year term life insurance policy locks in that rate for two full decades. The same person waiting until 40 could pay double for identical life insurance coverage. Buying young is the single most effective way to save on life insurance over the long run. And it is also the simplest action you can take.

Choose Term Life for Pure Income Replacement

If what you need is income replacement for your family during your working years term life insurance gives you the most life insurance coverage per dollar. The market offers term and permanent life insurance but for most families under 50 affordable term life is the smarter financial choice. You can always compare life insurance options later and convert if your needs change. There is no reason to pay for a permanent policy when a well-priced term plan does the job.

Quit Smoking at Least 12 Months Before Applying

Most life insurance companies in the U.S. reclassify applicants as non-smokers after 12 consecutive months without any tobacco use. That one change alone can drop your life insurance rates by 40 to 60 percent. It is one of the most impactful single actions any tobacco user can take before they get life insurance quotes from multiple carriers. The math on this is hard to argue with — a $90 monthly policy can drop to $29 just by quitting early enough.

Do Not Skip the Medical Exam If You Are Healthy

No-exam life insurance is convenient but it costs more. If you are in good health going through the life insurance medical exam usually gets you into a better health class and a meaningfully lower monthly rate. The exam itself is free and is usually done right at your home or office. For most healthy applicants in their 30s and 40s it is worth the small time investment to go through full underwriting.

Always Comparison Shop Across Multiple Carriers

Getting life insurance quotes from multiple insurers is one of the easiest ways to find a better rate. Carrier pricing models weight risk factors differently so two carriers can return very different numbers for the exact same applicant. Getting quotes from multiple companies through a comparison tool like the Life Insurance Quote Calculator is the most efficient way to find the best life insurance policy at the lowest available price. It takes about two minutes and costs nothing.

| Savings Strategy | Potential Rate Reduction | Who Benefits Most |

| Buy when young | Up to 50% vs waiting 10 years | Everyone under 40 |

| Choose term over permanent | 40-70% lower monthly cost | Families needing income replacement |

| Quit smoking 12+ months | 40-60% rate reduction | Current or former tobacco users |

| Take the medical exam | 10-25% vs no-exam pricing | Healthy applicants under 55 |

| Shop multiple carriers | 15-30% savings possible | All applicants |

Top 10 Life Insurance Companies in the USA — 2026 Rankings

Here is a clean look at how to think about the top 10 life insurance companies in the U.S. for 2026. Rather than naming specific brands, what the best carriers all share is a set of measurable qualities that you can use to evaluate any life insurer you are considering.

The strongest carriers in the U.S. insurance industry right now hold AM Best ratings of A or better and have NAIC complaint indexes well below 1.0. They offer a range of life insurance products that includes both term and permanent life insurance options. They make it easy to get life insurance quotes online and their claims processes are documented and transparent. That combination of financial strength, product range and customer accessibility is what separates the truly most reliable life insurance companies from the rest of the market.

When you are comparing any carrier against this standard, use the best life insurance calculators 2026 page to check how their rates stack up against the broader market. A well-rated carrier that prices 25 percent above the average for your profile is worth questioning even with a great AM Best score.

Worst Life Insurance Companies — Red Flags to Watch Out For

No blog about the best life insurance companies 2026 is complete without talking about what to avoid. There are carriers operating in the U.S. that have earned a reputation for slow claims, confusing policy language or complaint volumes well above the industry average. Knowing the red flags protects you just as much as knowing what to look for.

Warning Signs in Life Insurance Company Reviews

A high NAIC complaint index is the clearest data signal. The national association of insurance commissioners publishes complaint ratios annually for every carrier operating in the U.S. A ratio above 1.0 means the company gets more complaints than the industry average for its size. Look for carriers with a ratio well below 1.0. Also watch for repeated complaints about denied claims or unexplained premium increases in life insurance company reviews. Those patterns do not appear by accident.

What a Bad Claims Experience Looks Like

A bad claims experience usually follows a predictable pattern. The family files the claim. The company asks for documentation they never mentioned during the application. Then they delay or partially deny the payout citing fine print that was never clearly explained at the point of sale. This is exactly why life insurance companies that pay out reliably are so highly valued by real policyholders. The best carriers have documented payout rates above 95 percent and claims processes that are clear from day one.

How to Spot a Financially Weak Carrier Before You Apply

Check the AM Best rating before anything else. Then look at ratings from other agencies like S&P and Moody’s if they are available for that carrier. A life insurer with an AM Best rating below A- should be researched very carefully before you commit to any life insurance policy. Financial weakness in a carrier means there is a real risk the company may not be able to pay your family when the time comes. That is the one outcome this entire product is designed to prevent.

| Red Flag | What It Means | How to Verify |

| NAIC complaint ratio > 1.5 | Above average complaints for its size | Check naic.org |

| AM Best below B++ | Potential financial instability | Check ambest.com |

| No online quote option | Possible high-pressure sales tactics | Test their website directly |

| Vague policy language | Claim denials may be easier to execute | Request sample policy documents |

| Frequent rate hikes (UL policies) | Poor long-term financial management | Research policyholder forums |

Best Life Insurance Companies That Pay Out — Claims and Reliability Data

When you purchase a life insurance policy the whole point is that your family actually receives the money. So looking at which life insurance companies that pay out reliably is just as important as comparing premiums. A low monthly rate from a slow-paying carrier is not a deal. It is a risk.

What Claim Payout Rate Actually Means

Claim payout rate is the percentage of submitted death benefit claims that a carrier actually pays out. A rate of 98 percent means that out of 100 filed claims the company paid 98 of them. The other 2 percent were typically denied for reasons like policy lapses, misrepresentation on the application or claims filed outside the coverage period. The highest rated life insurance companies in the U.S. consistently maintain payout rates above 96 to 99 percent. That is the benchmark to measure any carrier against.

Which Companies Have the Strongest Claims Track Records

The most reliable life insurance companies in the U.S. share some common traits when it comes to claims. They have clear policy language that leaves little room for dispute at claim time. They have responsive claims teams that communicate proactively with beneficiaries. And they have the financial strength to pay without delay. Based on life insurance company reviews and publicly available data from the insurance industry the carriers that consistently rank highest for claims reliability are those holding AM Best ratings of A+ or A++ with NAIC complaint indexes below 0.30.

How to File a Life Insurance Claim Successfully

Filing a life insurance claim is simpler than most people fear. You contact the carrier directly and request a claim form. You will need the original policy document, the certified death certificate and proof of your identity as the named beneficiary. Submit everything together in one package. Most reputable life insurance companies process complete claims within 10 to 30 days of receiving all required documentation. Keep copies of everything you send and follow up in writing if you have not heard back within 14 days of submission.

How to Choose the Right Life Insurance Company for You

Choosing from so many life insurance providers does not have to feel like a puzzle. Follow these five steps and you will end up in a much stronger position than most people who just go with the first option they find.

Step 1 — Decide Which Type of Life Insurance Fits Your Life

If you need affordable coverage for a defined period while your kids grow up or your mortgage gets paid down term life insurance is almost always the right call for most U.S. families. If you want lifelong coverage with a cash component look at whole life insurance or universal life insurance policies. Most people shopping for individual life insurance policies for the first time belong squarely in the term life insurance options category based on age, income and family need.

Step 2 — Calculate the Coverage Amount You Need

Use either the DIME method or the income multiplier as your starting point. Then factor in any existing assets, savings or other life insurance policies you already hold. The goal is to identify the gap between what your family would have without your income and what they actually need to maintain their standard of living for the next 10 to 20 years.

Step 3 — Check AM Best Ratings Before You Apply

Once you have a list of life insurance companies you are considering look up their AM Best rating before doing anything else. Stick with carriers rated A- or higher. This step takes about five minutes and it removes the risk of placing a permanent life insurance policy with a financially shaky carrier. It is one of the simplest due diligence moves available to any U.S. buyer.

Step 4 — Get Quotes From Multiple Companies

Never go with the first quote you receive. Insurance policies in the U.S. are priced differently by every carrier even for identical applicants. Getting life insurance quotes from multiple carriers is the most reliable way to find the best life insurance policy for your budget and health profile. And it costs nothing to compare. The companies to find the best rate for your profile are rarely the ones you hear about first.

Step 5 — Use a Life Insurance Quote Calculator to Compare

The fastest way to compare life insurance across carriers is through a dedicated quote tool. The Life Insurance Quote Calculator lets you enter your age, health and coverage needs and instantly see life insurance rates from reputable life insurance companies without handing over your phone number or sitting through a sales pitch. It is free, takes under two minutes and gives you a real working number before you commit to anything.

| Step | Action | Tool or Resource | Time Required |

| 1 | Choose policy type | This blog post | 5 minutes |

| 2 | Calculate coverage needed | DIME or income multiplier | 10 minutes |

| 3 | Check AM Best ratings | ambest.com | 5 minutes |

| 4 | Get multiple quotes | Quote calculator | 2-3 minutes |

| 5 | Compare and apply | Life Insurance Quote Calculator | 10-15 minutes |

Frequently Asked Questions — Best Life Insurance Companies 2026

1. What is the best insurance to have in 2026

The truth is most people go with term life because it is simple and affordable. But whole life can work if you want long term value. For many people the best life insurance companies 2026 offer both so it depends on your goals.

2. What is the most reputable life insurance company

From what I have seen companies with strong AM Best ratings tend to be trusted more. Names like Northwestern Mutual or New York Life come up a lot. They have solid life insurance company ratings and long history.

3. Who is the number 1 life insurance company

There is no single number one for everyone. Some rank higher in life insurance company ranking based on size while others lead in service. The best life insurance companies 2026 vary based on what you need.

4. Which company has the best life insurance policy

It depends on policy type. Some companies lead in term plans while others in whole life. From my experience comparing policies is key because highest rated life insurance often changes by coverage type.

5. What company has the best life insurance rates

Rates depend on age health and lifestyle. Companies like Banner Life or Haven Life often offer low rates. But the best life insurance companies 2026 adjust pricing often so always compare quotes.

6. Top life insurance companies 2026

You will often see lists that include State Farm MassMutual Prudential and Guardian. These are among the most reliable life insurance companies in the USA with strong financial backing.

7. How much life insurance do I need

A simple rule is ten times your yearly income. But honestly it depends on debts family needs and future goals. I usually suggest calculating your expenses first then picking coverage.

8. How much does life insurance cost per month on average

For a healthy adult term life can cost as low as 20 to 50 dollars per month. Whole life costs more. The best life insurance companies 2026 offer flexible plans so prices vary a lot.

9. Can I get life insurance without a medical exam

Yes you can. No exam policies are quick and easy. But they usually cost more. Still many reputable life insurance companies now offer this option for convenience.

10. Term life vs whole life insurance Which is better

Term life is cheaper and good for temporary needs. Whole life builds cash value over time. So the better option depends on your financial plan and how long you need coverage.

Use the Life Insurance Quote Calculator to Find Your Best Rate Today

You now have a clear picture of the best life insurance companies 2026, how rates compare across age and health profiles, what the different life insurance options actually offer and how to avoid the carriers that fall short on claims. The information here covers everything from cheapest life insurance companies to the most reputable life insurance companies with the strongest payout track records.

The next step is simple. Get your own number. Use the Life Insurance Premium Calculator to see real 2026 rates based on your age, health and coverage goals. No phone number required. No sales pressure. Just your real rate in under two minutes. And if you want to go deeper before deciding, these related reads on the blog will help: How Does Life Insurance Work and Term vs Whole Life Insurance and How Is Life Insurance Calculated