Explore life insurance for women, compare policy types, understand costs, and find the best coverage to protect your income, family, and future. Use our Life Insurance Quote Calculator to see your rates

Table of Contents

Life Insurance for Women

Life insurance for women is no longer a choice it is a necessity. Today’s women are business owners, breadwinners, caregivers, and decision-makers. You may be married, single, a mom, or in the early stages of your career. Regardless of your circumstances, life insurance for women is a must-have to protect your loved ones from uncertainty.

Traditionally, people have thought that only the primary breadwinner in the family needs life insurance. That is no longer true. Women play a significant role in driving the economy forward.

Understanding Life Insurance for Women: Key Differences and Benefits

Life insurance for women works much like any standard life insurance policy, but there are some important differences to keep in mind. On average, women tend to live longer than men, which can influence the way policies are structured and the benefits they offerThis means that life insurance for women tends to be relatively cheap.

Another factor to be taken into consideration while opting for women life insurance policy

is the medical history. Various insurance companies take into account the age factor, medical background, lifestyle, and maternity issues while offering life insurance quotes for women. Since women have a longer life expectancy, they can enjoy competitive life insurance quotes for women.

The benefits of women life insurance policy

go beyond the replacement of income. Funeral expenses, loan repayments, mortgage payments, children’s education funds, estate planning, etc., can also be covered through life insurance for women.

Whether you need women life insurance policy

or life insurance quotes for women, the right policy will give you peace of mind. It’s not just about the worst-case scenario. It’s about everything you’ve worked for.

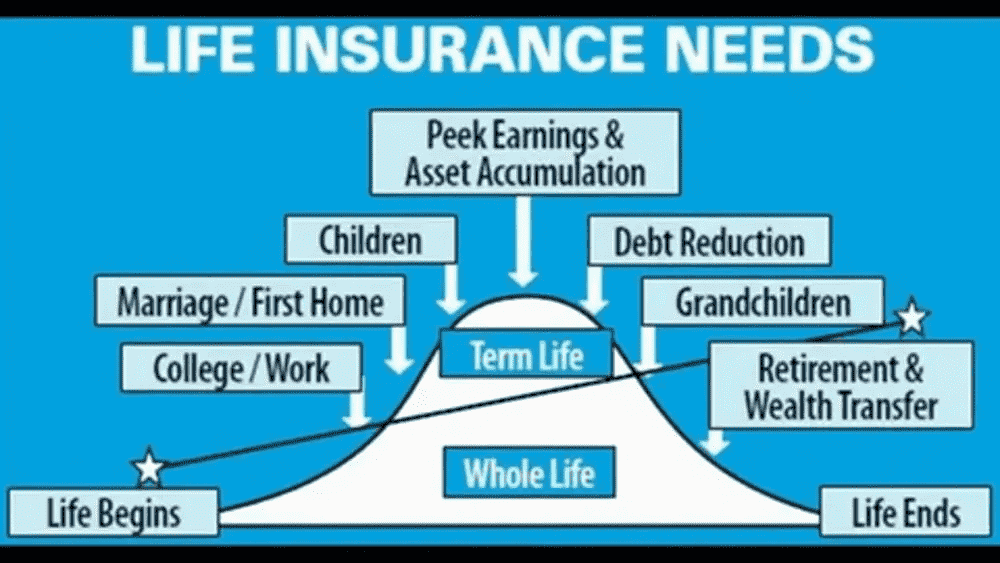

Types of Life Insurance for Women

Term life insurance coverage for women

Term life insurance for women covers the policyholder for a specified period, such as 10, 20, or 30 years. Term life insurance is the cheapest life insurance for women. It is best for income replacement during the working years or for the duration of the family-raising years.

Whole women insurance plans

Whole life insurance for women covers the policyholder for her entire life. It has a cash value component. Although it is more expensive, it is best for estate planning or leaving a guaranteed inheritance for the family.

Universal Life Insurance

Universal life insurance is best for women due to the flexibility it offers. You can vary the death benefit and premiums. It is best for women’s life insurance, as it is flexible.

How Much Life Insurance Coverage Do Women Need?

To calculate the right amount of cheap life insurance for women

, there are a few things to keep in mind. A general rule of thumb is to multiply the sum by 10 to 15 times the income earned. However, this is just the beginning.

You should factor in the debts, mortgages, future education costs for the kids, and the contributions made at home. Stay-at-home moms should calculate the costs of hiring someone to take care of the kids, transportation, and the management of the home.

When it comes to female life insurance rates

it is important to remember that it is not just the financial contributions that are important. Life insurance for women should provide the right balance of financial security, regardless of whether the woman is single or married.

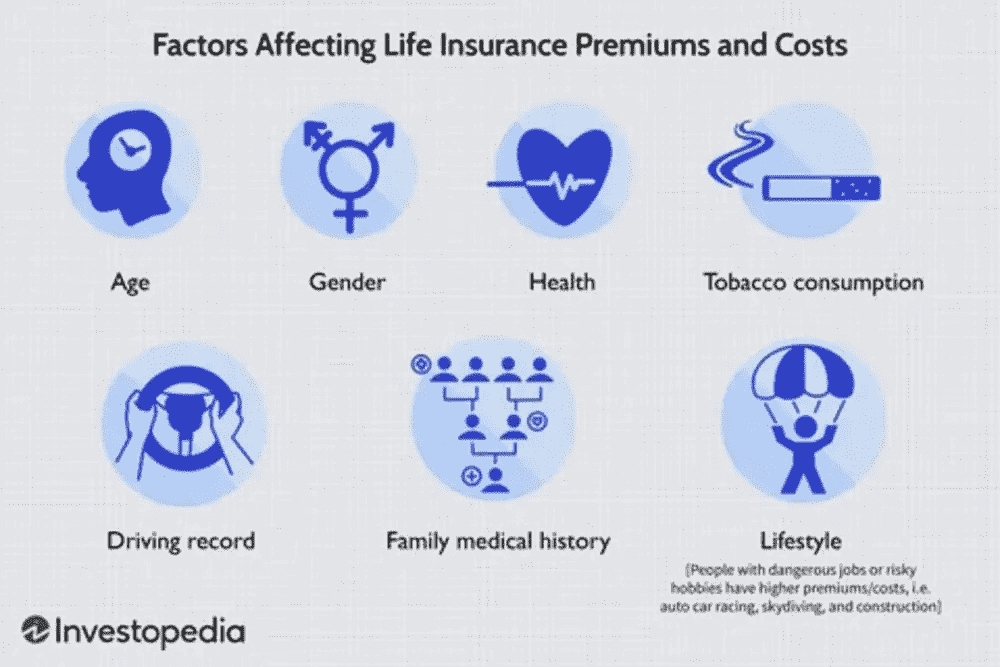

Factors That Affect the Cost of income protection for women

| Factor | Impact on Life Insurance Rates for Women |

|---|---|

| Age | The earlier you buy lbest insurance companies for women , the lower the premiums you can expect to pay. |

| Health | Lifestyle diseases, smoking habits, and high-risk lifestyles can increase premiums. |

| Coverage Amount | The more you wish to insure your life for, the higher the premiums you can expect to pay. |

| Policy Type | Term life insurance policies for women generally offer lower premiums compared to whole life insurance policies for women. |

| Insurance Provider | Different insurance providers may charge different premiums based on their risk assessment policies. |

Special Considerations: Mothers, Single Women & Working Professionals

Mothers need coverage for the future expenses of the children and the daily expenses.

For single mothers, the need for replacement of income or education funding should be the priority.

For stay-at-home mothers, the need to cover the economic value of unpaid work should be a priority.

For working women, the need for coverage for long-term financial planning or business continuation should be a priority.

Although single women without dependents need llife insurance for working women

they need it to avoid imposing additional expenses on the family.

How to Choose the Best Life Insurance Policy

Choosing life insurance as a single mother can feel overwhelming, but it becomes much easier when you know what to look for. Start by clearly understanding your financial responsibilities, goals, and budget—this will help you find a policy that truly fits your needs.

Once you know what you need, take the time to compare quotes from different insurance providers. Look beyond the price—consider how flexible the policy is, whether the premiums remain stable over time, and the insurance company’s track record when it comes to paying claims. These factors can make a big difference in ensuring that you and your family are properly protected.

While the cost of the policy is an important factor to be considered while choosing the right income protection for womenyou need to be careful not to compromise on the coverage amount while choosing the most cost-effective life insurance policy for women.

In case you need help choosing the right women financial protection

FAQs

1. Is financial protection for women cheaper than for men?

Yes, in many cases. Women often receive lower life insurance rates due to longer life expectancy.

2. When should women buy life insurance?

The earlier, the better. Buying life insurance for women at a younger age locks in lower premiums.

3. Do stay-at-home moms need life insurance?

Absolutely. Replacing childcare and household management services can be expensive.

4. Can pregnant women qualify for coverage?

Yes. Most insurers offer life insurance for women during pregnancy, though medical history is reviewed.

5. How much life insurance coverage is enough?

It depends on income, debts, and financial goals. A personalized assessment ensures proper protection.

Conclusion

Life insurance for women is a smart and essential step toward financial security. Whether you’re earning, caregiving, or managing a household, the right coverage protects your loved ones from unexpected financial hardship. With affordable options and lower life insurance rates available to many women, securing a policy early can provide long-term peace of mind. Simply put, life insurance for women ensures your family’s stability, safeguards your future plans, and gives you confidence that everything you value is protected.

2 Comments

[…] In this guide, we will be able to assist you in better understanding the way in which you can obtain a life insurance policy. […]

[…] truckers believe that they cannot acquire life insurance because of the nature of the job. However, the insurance companies assess many other factors besides […]